Notice is hereby given that a Meeting of

the Around the Mountains Cycle Trail Project Subcommittee will be held on:

|

Date:

Time:

Meeting Room:

Venue:

|

Tuesday, 27

September 2016

3.00pm

Council Chambers

15 Forth Street

Invercargill

|

|

Around the Mountains Cycle Trail Project

Subcommittee Agenda

OPEN

|

MEMBERSHIP

|

Chairperson

|

Lyall Bailey

|

|

|

|

Mayor Gary Tong

|

|

|

Councillors

|

Brian Dillon

|

|

|

|

Rodney Dobson

|

|

|

|

Paul Duffy

|

|

|

|

Ebel Kremer

|

|

IN ATTENDANCE

|

Group Manager Services and Assets

|

Ian Marshall

|

|

Committee Advisor

|

Fiona Dunlop

|

Terms of

Reference for the Around the Mountains Cycle Trail Project Subcommittee

This subcommittee is a subcommittee of Activities

Performance Audit Committee and has responsibility for:

·

Project Completion - To ensure the cycle trail

project is completed to the standard expected on a no surprises basis, by

(i) Monitoring

progress and making decisions to allow completion to be achieved.

·

Project Progress - To monitor progress of the

project and make necessary decisions to keep the project on track in accordance

with the project plan. To ensure the project is completed on time in accordance

with the project plan, by

(i) Receive sufficiently detailed

progress reports from the Project Manager to be able to be fully informed of

progress towards the completion outcome

(ii) Making decisions on actions necessary

to overcome constraints that put achieving the planned outcome at risk.

·

Financial Management - To ensure the project is

completed to the agreed budget, by

(i) Receiving sufficiently detailed

progress reports from the Project Manager to be able to be fully informed of

the likely completion outcome

(ii) Making decisions on actions

necessary to overcome constraints that put achieving the completion within

budget at risk

(iii) Approving Procurement Plans and Let

Contracts in accordance with those plans for the purchase of goods and services

to complete the cycle trail project.

·

Risk Management - To monitor Risk Management

processes and ensure that risks are being identified, mitigated and managed, by

(i) Receiving reports on risk

management, assessing if all important risks are being managed properly

(ii) Flagging any unmanaged risks.

·

Health and Safety Management - To monitor Health

and Safety management and ensure it is being carried out appropriately, by

(i) Receiving reports on Health and

Safety management including evidence of proactive management and evidence of

safety observations and due diligence.

(ii) Ensuring unsafe practices are

eliminated from the project.

·

Compliance - To monitor consent compliance to

ensure all work is carried out under necessary consents and to ensure all

consent conditions are complied with, by

(i) Receiving confirmation reports of

consent compliance

(ii) Receiving exception reports on issues

of non-compliance and proposals to correct non-compliance.

|

Around the Mountains Cycle Trail Project Subcommittee

27 September

2016

|

|

TABLE OF

CONTENTS

ITEM PAGE

Procedural

1 Apologies 5

2 Leave of

absence 5

3 Conflict of

Interest 5

4 Public Forum 5

5 Extraordinary/Urgent

Items 5

6 Confirmation

of Minutes 5

Reports for Recommendation

7.1 Around

the Mountains Cycle Trail Review Action Plan 7

Reports

8.1 Financial

Report to 30 June 2016 17

Public Excluded

Procedural motion

to exclude the public 21

C9.1 Legal

Advice on Appeal process and Claim for Costs 21

At the close of

the agenda no apologies had been received.

2 Leave

of absence

At the close of

the agenda no requests for leave of absence had been received.

3 Conflict

of Interest

Committee

Members are reminded of the need to be vigilant to stand aside from

decision-making when a conflict arises between their role as a member and any

private or other external interest they might have.

4 Public Forum

Notification to

speak is required by 5pm at least two days before the meeting. Further

information is available on www.southlanddc.govt.nz

or phoning 0800 732 732.

5 Extraordinary/Urgent

Items

To consider, and if

thought fit, to pass a resolution to permit the committee

to consider any further items which do not appear on

the Agenda of this meeting and/or the meeting to be held with the public

excluded.

Such resolution is

required to be made pursuant to Section 46A(7) of the Local Government Official

Information and Meetings Act 1987, and the Chairperson must advise:

(i) the

reason why the item was not on the Agenda, and

(ii) the

reason why the discussion of this item cannot be delayed until a subsequent

meeting.

Section 46A(7A) of the Local Government Official Information and Meetings

Act 1987 (as amended) states:

“Where an item

is not on the agenda for a meeting,-

(a)

that item may be discussed at that meeting if-

(i) that

item is a minor matter relating to the general business of the local authority;

and

(ii) the

presiding member explains at the beginning of the meeting, at a time when it is

open to the public, that the item will be discussed at the meeting; but

(b)

no resolution, decision or recommendation may be made in respect

of that item except to refer that item to a subsequent meeting of the local

authority for further discussion.”

6 Confirmation

of Minutes

6.1 There are no minutes to confirm.

|

Around the

Mountains Cycle Trail Project Subcommittee

27 September

2016

|

|

Around the

Mountains Cycle Trail Review Action Plan

Record No: R/16/9/15047

Author: Steve

Ruru, Chief Executive

Approved by: Steve Ruru,

Chief Executive

☐

Decision ☒

Recommendation ☐

Information

Purpose

1 To

seek a recommendation from the Subcommittee to recommend adoption of the

proposed Action Plan which has been developed in response to the findings from

the Deloitte review of the way in which Council has managed the financial

aspects of the Around the Mountain Cycle Trail (ATMCT) project.

Executive

Summary

2 Deloitte

have recently completed their review of the way in which Council has managed

the financial aspects of the ATMCT. The report identifies a number of issues

with the way in which the project was managed. To ensure that the organisation

takes on board the lessons to be learnt from the review it is seen as

appropriate for a structured Action Plan to be put in place.

3 The

Action Plan attached to this report outlines the actions proposed to respond to

the report’s findings. While a number of these relate specifically to the

ATMCT project a number also apply to the organisation as a whole.

|

Recommendation

That the Around the

Mountains Cycle Trail Project Subcommittee:

a) Receives

the report titled “Around the Mountains Cycle Trail Review Action

Plan” dated 21 September 2016.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Agrees

to recommend to the Activities Performance Audit Committee that it approves

the Improvement Action Plans attached to this report.

e) Recommends

to the Activities Performance Audit Committee that it asks officers to report

back to the Committee on a six monthly basis with an update on progress in

implementing the agreed actions.

|

Content

Background

4 At

its 9 December 2015 meeting the Activities Performance Audit Committee (APAC)

agreed to commission an independent review of the way in which Council has

managed the financial aspects of the ATMCT. Deloitte were subsequently

appointed to undertake the review. A copy of the draft Deloitte report was

considered by Council at its 20 July 2016 meeting at which time they asked

officers to report to APAC with a proposed Action Plan to address the actions,

including improvement opportunities, which should be taken in response to the

report.

Issues

5 There

is a need for this Subcommittee to consider the draft Action Plan attached and

determine whether it addresses all of the actions and improvement opportunities

which it considers should be addressed.

6 In

developing the Action Plan officers have had regard to the Deloitte Project

Quality Assurance Framework which is outlined in section 10 of the Deloitte

report. Officers have also split the plan into actions that they believe should

be taken in relation to the ATMCT project and those which apply more

generically to organisational processes.

Factors to Consider

Legal

and Statutory Requirements

7 The

proposal to develop an Action Plan, including identifying improvement options,

is consistent with Council’s obligations under the Local Government Act

2002 to manage its business in a prudent and business-like manner.

Community

Views

8 The

community would expect Council to address the issues arising out of the

Deloitte review via a structured action plan. In this way they can be assured

that the organisation has learnt from the short-comings identified and that

there is an appropriate level of accountability for the short-comings

identified.

Costs

and Funding

9 The

costs associated with implementation of the Action Plan will be funded from

within existing budgets.

Policy

Implications

10 There

are no direct policy implications coming out of approving the proposed Action

Plan. Some of the proposed actions may lead to changes being proposed to

current policies. These will be identified at that time.

Analysis

Options Considered

Option 1 – Implement an

Action Plan

11 Under

this option the Subcommittee would, subject to any modifications that they wish

to see made, recommend to APAC that it approve the Action Plan attached.

12 Officers

would then report back to APAC on a regular basis to enable that Committee to

monitor the progress being made in implementing the actions identified.

Option 2: Do Nothing

13 Under

this option the Subcommittee would determine that no further action is required

and recommend to APAC that it not approve the Action Plan attached. A number of

the improvement opportunities flowing out of the review could be implemented

but on a more ad hoc basis.

Analysis of Options

Option

1 – Implement an Action Plan

|

Advantages

|

Disadvantages

|

|

· Council

can take the actions, including improvements considered necessary, in

response to the Deloitte review via a structured plan.

· Council

can ensure that the lessons which need to be learnt from this review are

implemented in a structured way.

· Risks

associated with completing the ATMCT and other projects will be reduced.

|

· There

will be costs associated with implementing the action plan albeit that these

will be absorbed within existing budgets.

|

Option

2 – Do Nothing

|

Advantages

|

Disadvantages

|

|

· Avoids

costs of implementing the actions identified.

|

· Any

improvement actions will be implemented in an ad hoc manner.

· Risk

of similar mistakes being made in the future will be increased.

· Council

will not be seen as having taken an appropriate set of actions in response to

the Deloitte review.

|

Assessment of Significance

14 This

report addresses the question of whether Council should put in place a plan to

address the short-comings identified through the Deloitte review. While there

will be a level of community interest in ensuring that Council takes

appropriate actions officers are of the view that a decision to adopt the Action

Plan would not be a significant decision.

Recommended

Option

15 It

is recommended that the Subcommittee adopt Option 1 and recommend to APAC that

it approve, subject to any changes the Committee may wish to make, the attached

Action Plan.

Next

Steps

16 The

recommendation of this Subcommittee will be provided for APAC for that

Committee to consider when reviewing the draft Action Plan.

ATMCT Action Plan

|

Project

Assurance Framework/Improvement Action

|

Current

Status

|

Improvement

Programme

|

Timeframe

|

Comment

|

|

Project

Governance

There

is a need to have a clearly defined project governance structure in place

that has the skills necessary to manage the project.

|

An

ATMCT Project Sub-committee is in place as a sub-committee of APAC to provide

governance oversight for the project through to completion.

|

Confirm

establishment of the Project Sub-Committee and the overall Project Management

structure to be used for remainder of the project.

|

November

2016

|

All

Council committees are, by law, disestablished at the end of each triennium.

As a result Council will need to re-establish the committee and approve its

terms of reference following completion of the triennial election.

This

will provide an opportunity to confirm the overall governance and project

management structure that is appropriate for the remainder of the capital

development phase of the project.

|

|

Resource

Management

It

is important to ensure that the project has access to the skills and level of

resources that it needs.

|

The

project currently has access to a range of internal and external resources to

drive the project.

|

Review

the range and quantum of resources allocated to the project as part of the

review of project governance and management structure.

|

Four

months after release of Environment Court decision.

|

|

|

Risk/Issues

Management

It

is important to identify and appropriately manage project risks.

|

A

number of project risks are being identified but have not been formally

reported through to APAC and/or the Project Steering Committee.

|

Ensure

that the Project Risk Register is developed and reported through to the

Project Governance Committee.

|

Each

Project Committee Meeting.

|

Register

will be developed in accordance with the Council Risk Management

Policy.

|

|

Probity

Auditor

|

A

probity auditor has not been appointed to date.

|

Consider

whether a Project Assurance/Probity Auditor should be appointed to provide

extra assurance over remaining stages of the project.

|

Four

months after release of the Environment Court decision.

|

Decision

will need to have regard to the procurement approach used for the final

stages of the project.

|

|

Financial

Management

Ensure

regular financial reports and financial reforecasts are produced for the

project through to completion.

|

New

financial reforecasts for the project were developed in 2015 given the change

in project status.

|

Ensure

financial report is provided to each meeting of the Project Sub-Committee.

Financial

reforecasts to be produced twice per year or as required to reflect a

significant change in project status.

|

October

and April.

|

Financial

reforecasts will be completed quarterly as per current organisational policy.

|

|

Procurement

Strategy

Develop

procurement strategy and business case for progressing completion of the

Trail.

|

Projections

have been developed for completing trail based on existing resource

consent.

|

Develop

business case addressing costs and benefits of proceeding with development of

remainder of the Trail once the Environment Court decision is released.

Develop

a procurement strategy detailing the nature of the contract proposed to be

used for remaining stages of the contract.

|

Four

months after release of the Environment Court decision.

|

The

projected cost of completing the ATMCT could change significantly following

release of the Environment Court decision.

It

will also be appropriate to review the procurement approach to be used given

that Council now has a significant level of information relating to the

likely construction costs and risks.

|

|

Operating

Model

|

Council

currently has a contract for operation of ATMCT booking system.

|

Review

the proposed Operating Model and financial projections for future operation

and maintenance of the ATMCT.

|

June

2017

|

Current

trail operating model and financial projections were developed in 2009. It is

therefore appropriate for them to be updated to reflect current knowledge.

|

|

|

|

|

|

|

Council Action Plan

|

Action

|

|

Current

Status

|

Improvement

Programme Action

|

Timeframe

|

Comment

|

|

Accountability

Workstream

Review

accountability options

|

|

|

Report

to Council on options for ensuring steps are implemented to enforce an

appropriate level of accountability for the short-comings identified through

the report.

|

April

2017

|

Report

will cover different parties that have been involved with the project.

|

|

Governance

Structure

Separate

Audit Committee and Services and Assets Committee functions

|

|

APAC

currently performs the role of being both an Audit Committee and an

Operations Committee.

|

Recommend

to Council the establishment of a separate Audit Committee and Services and

Assets Committee.

|

November

2016

|

Audit

Committee should be established in a manner that is consistent with good

practice. Revised terms of reference and work programme would be developed as

part of the new approach.

|

|

Risk

Management

Internal

Audit programme

|

|

Council

is part of a South Island internal audit pilot programme.

|

Develop

Internal Audit programme based on organisational risk profile.

|

June

2017

|

Review

of pilot and other options is needed.

|

|

Review

operation of risk management policy

|

|

Risk

Management Policy has been operational for eighteen months.

|

Review

operation of existing risk management policy.

|

March

2017

|

|

|

Procurement

and Contract Management Strategy

|

|

Project

has been scoped and is currently underway.

|

Develop

Procurement, Project and Contract management Framework.

|

December

2017

|

Project

scope and current status report will be bought to APAC in November.

|

Attachments

There are no attachments for

this report.

|

Around the

Mountains Cycle Trail Project Subcommittee

27 September

2016

|

|

Financial

Report to 30 June 2016

Record No: R/16/9/14775

Author: Anne

Robson, Chief Financial Officer

Approved by: Steve Ruru,

Chief Executive

☐

Decision ☐

Recommendation ☒

Information

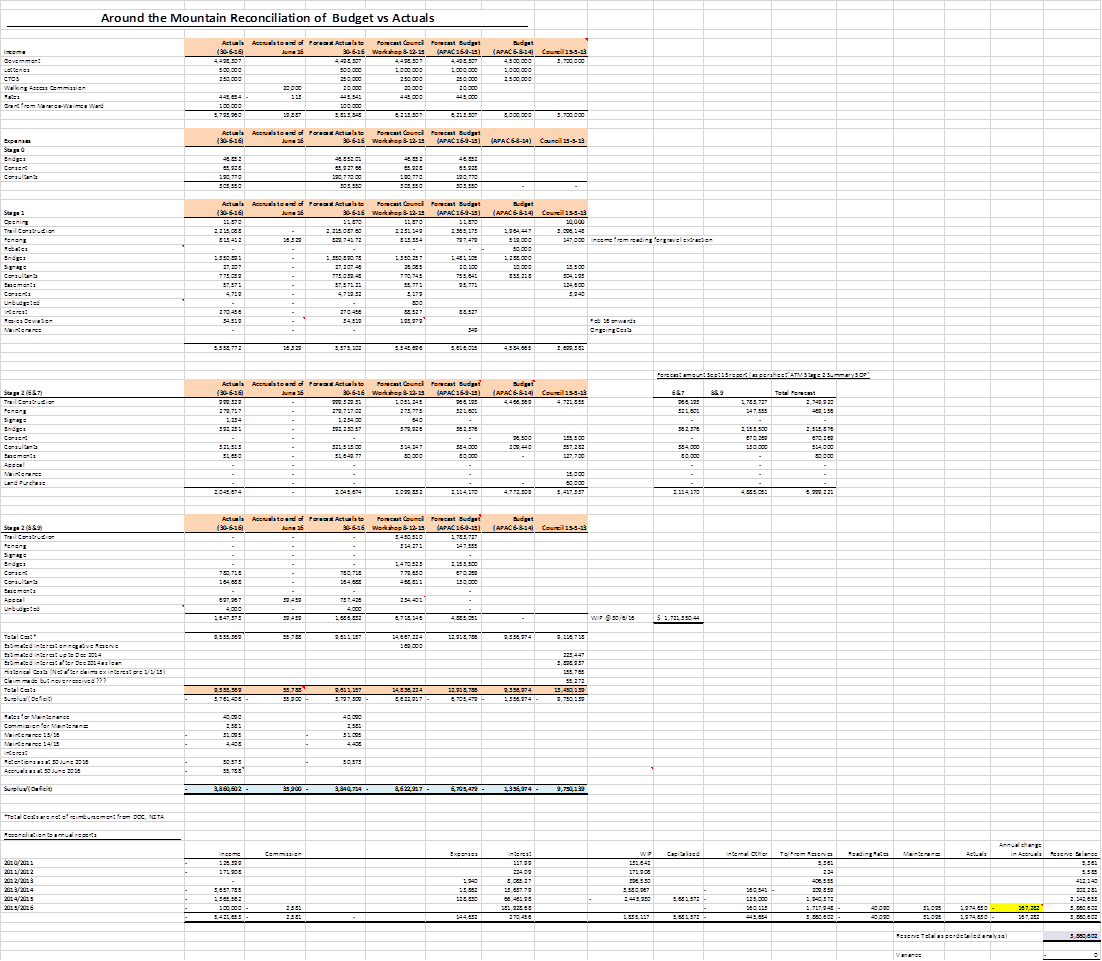

1 This

report summarises the financial position of the Around the Mountains Cycle

Trail to 30 June 2016 for costs incurred/accrued to date against budget.

2 Attached

is the full financial reconciliation of costs for the project to the notified

budgets of Council. The below is a summary of this document comparing

actual costs to the council budget of 8 December 2015.

|

|

Actual

Costs to 30 June 2016

|

Budget Council Workshop 8-12-15

|

Key Variance (under)/over

|

Notes

|

|

Income

|

5,793,960

|

6,213,307

|

(419,347)

|

1

|

|

|

|

|

|

|

|

Less Expenses

|

|

|

|

|

|

Stage 0

|

303,550

|

303,550

|

|

|

|

Stage 1 (incl interest on

negative reserve)

|

5,575,102

|

5,714,696

|

(139,594)

|

2

|

|

Stage 2 (sections 6&7 plus

retentions)

|

2,096,247

|

2,099,832

|

|

|

|

Stage 2 (Sections 8&9)

|

1,686,832

|

6,718,146

|

(5,031,314)

|

3

|

|

Total Costs

|

9,661,731

|

14,836,224

|

|

|

|

Net Deficit

|

3,867,771

|

8,622,917

|

|

|

|

Less Operating Cost net surplus

|

7,168

|

|

|

|

|

Balance of Reserve at 30 June

2016

|

($3,860,603)

|

|

|

|

3 Note

1, an analysis of the income variation is as follows:

|

Entity

|

Key

Variance

|

Notes

|

|

Lotteries Commission

|

500,000

|

An extension to apply for the balance of funding

has been received from the Lotteries Commission until 31 December 2018.

|

|

Walking Access Commission

|

20,000

|

On completion of registering access rights on

titles, this grant will be received.

|

|

Grant from Mararoa-Waimea Ward

|

(100,000)

|

A contribution towards signage and other costs

of the trail was received from the Mararoa Waimea ward. This was unbudgeted.

|

|

|

$420,000

|

|

4 Note

2, of the $139,594 variance, $159,460 relates to the completion of the property

deviation that is in progress. To date $34,519 has been spent of a budgeted

$193,979. It is expected that the final cost will come within the

budget. Additionally, fencing has come in $16,407 over budget due to

additional fencing being undertaken on Menlove’s property in the area of

the deep railway cutting. When the fencing programme was initially

planned it was thought stock would not create a problem in this area.

However, this has proven not to be the case and in order to prevent ongoing

maintenance problems and conflict with stock issues it was decided that it was

prudent to fence this section.

5 Note

3, Stage 2 (sections 8 & 9) is broken down as follows:

|

|

Actual

Costs to 30 June 2016

|

Budget

Council Workshop 8-12-16

|

Variance

under/(over)

|

|

Consent & Appeal Costs

|

1,518,144

|

1,014,031

|

(504,113)

|

|

Consultants

|

168,688

|

468,811

|

(300,123)

|

|

Construction 8&9

|

-

|

5,704,115

|

5,704,115

|

|

Total

|

1,686,832

|

7,186,957

|

|

6 The

Consent & Appeal costs are over budget by $504,113. Only one invoice

in relation to final legal advice is to be received and will add to the overall

actual cost. All other costs in relation to the Environment Court process

have been received.

7 Consultant

costs incurred to date are in relation to design work to inform the appeal

process. This work has also been of benefit to further define the scope

of works for sections 8 & 9.

8 Until

the Environment Court decision is released and Council has had the time to

consider the decision and any conditions and make a decision on the next steps,

no work is/will be undertaken in revising the estimated consultants and

construction costs of sections 8 & 9.

|

Recommendation

That the Around the

Mountains Cycle Trail Project Subcommittee:

a) Receives

the report titled “Financial Report to 30 June 2016” dated 21

September 2016.

|

Attachments

a Around

the Mountains Cycle Trail 30 June 2016 Financial Report, Financial Attachment ⇩

|

Around the

Mountains Cycle Trail Project Subcommittee

|

27 September 2016

|

|

Around the Mountains Cycle Trail Project Subcommittee

27 September

2016

|

|

Exclusion of the Public: Local Government Official Information and

Meetings Act 1987

|

Recommendation

That the

public be excluded from the following part(s) of the proceedings of this

meeting.

C9.1 Legal

Advice on Appeal process and Claim for Costs

The general

subject of each matter to be considered while the public is excluded, the

reason for passing this resolution in relation to each matter, and the

specific grounds under section 48(1) of the Local Government Official

Information and Meetings Act 1987 for the passing of this resolution are as

follows:

|

|

General subject of each matter to be considered

|

Reason for passing this resolution in relation to

each matter

|

Ground(s) under section 48(1) for the passing of this

resolution

|

|

Legal Advice on Appeal process and Claim for Costs

|

s7(2)(g) - The withholding of the information is

necessary to maintain legal professional privilege.

|

That the public conduct of the whole or the relevant

part of the proceedings of the meeting would be likely to result in the

disclosure of information for which good reason for withholding exists.

|