Notice is hereby given that an Ordinary

Meeting of Southland District Council will be held on:

|

Date:

Time:

Meeting Room:

Venue:

|

Wednesday, 28

September 2016

9am

Council Chambers

15 Forth Street

Invercargill

|

|

Council Agenda

OPEN

|

MEMBERSHIP

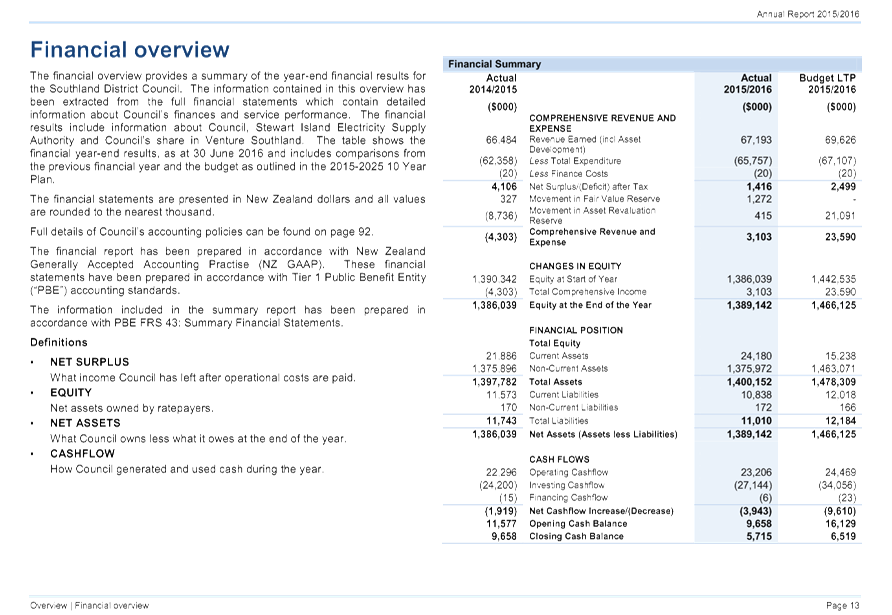

|

Mayor

|

Mayor Gary Tong

|

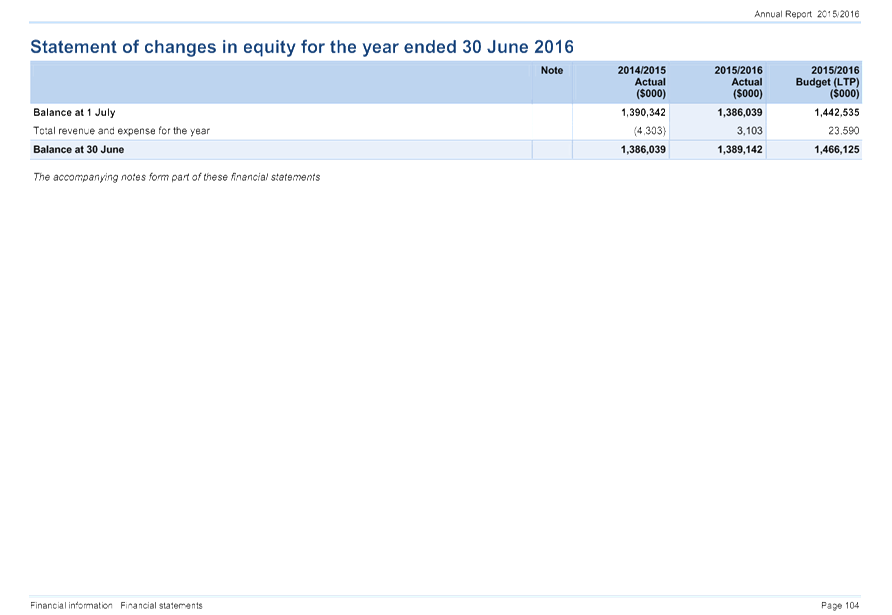

|

|

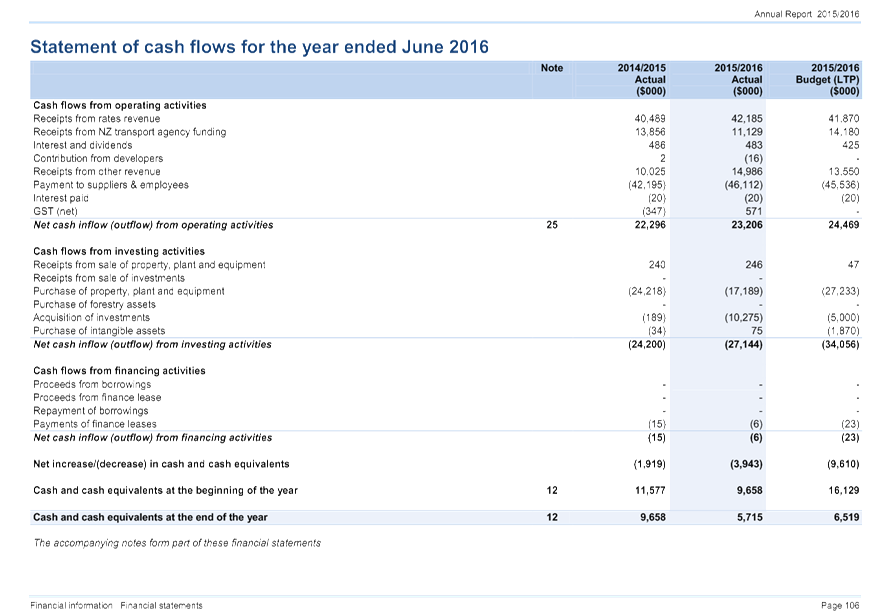

Deputy Mayor

|

Paul Duffy

|

|

|

Councillors

|

Lyall Bailey

|

|

|

|

Stuart Baird

|

|

|

|

Brian Dillon

|

|

|

|

Rodney Dobson

|

|

|

|

John Douglas

|

|

|

|

Bruce Ford

|

|

|

|

George Harpur

|

|

|

|

Julie Keast

|

|

|

|

Ebel Kremer

|

|

|

|

Gavin Macpherson

|

|

|

|

Neil Paterson

|

|

IN ATTENDANCE

|

Chief Executive

|

Steve Ruru

|

|

|

Committee Advisor

|

Fiona Dunlop

|

|

|

Council

28 September

2016

|

|

TABLE OF CONTENTS

ITEM PAGE

Procedural

1 Apologies 5

2 Leave of

absence 5

3 Conflict of

Interest 5

4 Public Forum 5

5 Extraordinary/Urgent

Items 5

6 Confirmation

of Council Minutes 5

Reports - Policy and Strategy

7.1 Adoption

of the Annual Report 2015/2016 7

7.2 Annual

Plan Timetable 2017/2018 191

7.3 Mediation

of the Appeals on the Proposed Southland District Plan 2012 - Delegated

Authority 197

7.4 Draft

Reserves Management Policy 201

Reports - Operational Matters

8.1 Council

Interest in Land Delegation 219

8.2 Alteration

to Unbudgeted Expenditure Approval for Winton Memorial Hall 221

8.3 Enhancements

to Council's Budgeting System 225

8.4 Delegation

of Authority to Chief Executive 231

Reports - Governance

9.1 Minutes

of the Riversdale Community Development Area Subcommittee Meeting dated 25 May

2016 235

9.2 Minutes

of the Balfour Community Development Area Subcommittee Meeting dated 25 May

2016 237

Public Excluded

Procedural motion

to exclude the public 239

C10.1 Milford

Sound Development Authority Annual Report 241

C10.2 Chief

Executive's Performance Review 279

VALEDICTORY SPEECHES

|

Council

28 September

2016

|

|

1 Apologies

At the close of

the agenda no apologies had been received.

2 Leave

of absence

At the close of

the agenda no requests for leave of absence had been received.

3 Conflict

of Interest

Councillors are

reminded of the need to be vigilant to stand aside from decision-making when a

conflict arises between their role as a councillor and any private or other

external interest they might have.

4 Public Forum

Notification to

speak is required by 5pm at least two days before the meeting. Further

information is available on www.southlanddc.govt.nz

or phoning 0800 732 732.

5 Extraordinary/Urgent

Items

To consider, and if

thought fit, to pass a resolution to permit the Council to consider any further

items which do not appear on the Agenda of this meeting and/or the meeting to

be held with the public excluded.

Such resolution is

required to be made pursuant to Section 46A(7) of the Local Government Official

Information and Meetings Act 1987, and the Chairperson must advise:

(i) The

reason why the item was not on the Agenda, and

(ii) The

reason why the discussion of this item cannot be delayed until a subsequent

meeting.

Section 46A(7A) of the Local Government Official Information and Meetings

Act 1987 (as amended) states:

“Where an item

is not on the agenda for a meeting,-

(a)

that item may be discussed at that meeting if-

(i) that

item is a minor matter relating to the general business of the local authority;

and

(ii) the

presiding member explains at the beginning of the meeting, at a time when it is

open to the public, that the item will be discussed at the meeting; but

(b)

no resolution, decision or recommendation may be made in

respect of that item except to refer that item to a subsequent meeting of the

local authority for further discussion.”

6 Confirmation

of Council Minutes

6.1 Meeting

minutes of Council, 7 September 2016

|

Council

28 September

2016

|

|

Adoption of

the Annual Report 2015/2016

Record No: R/16/9/14486

Author: Katherine

McDonald, Corporate Planning and Performance Advisor

Approved by: Steve Ruru,

Chief Executive

☒

Decision ☐

Recommendation ☐

Information

Purpose

1 Adoption of the

Annual Report is required under the Local Government Act 2002.

2 The

Annual Report is a means for Council to account and report to the community on

its performance of the preceding financial year. It reports on outcomes,

performance measures, both financial and non-financial and provides the actual

results against budgeted results. This Annual Report reports against the

first year of the Council’s 10 Year Plan 2015-2025.

Executive

Summary

3 Council

staff have compiled the Annual Report for the financial year ended 30 June

2016. The report has been reviewed by members of the Executive Leadership

Team. Additionally, a draft unaudited Annual Report was presented to a

Council workshop on 7 September 2016 for consideration and comment. These

comments have been noted and incorporated into the Annual Report.

4 Audit

New Zealand staff were onsite at Council from 5-16 September 2016 and have

completed the majority of their review of the Annual Report and the summary

document.

As such these documents may be subject to change and any changes will be

outlined at the meeting.

5 Audit

New Zealand Director, Mr Ian Lothian is anticipating attending Council’s

meeting on

28 September to present the audit opinion to Council.

6 As

with previous years, both an Annual Report and an Annual Report summary

document have been produced. The Annual Report and the Annual Report

summary document will be available at Council offices and on the Council

website. A printed copy is also distributed to those on the Council

mailing list.

7 The summary

document will be tabled and distributed at the meeting on 28 September 2016.

|

Recommendation

That the Council:

a) Receives

the report titled “Adoption of the Annual Report 2015/2016” dated

21 September 2016.

b) Determines

that this matter or decision be recognised as significant in

terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Adopts

the Annual Report and Annual Report Summary Document for the year ended 30

June 2016.

e) Delegates

authority to the Chief Executive to approve any minor amendments needed to

these documents subsequent to this meeting.

f) Delegates

authority to the Chief Executive and Mayor to sign the letter of

representation to Audit New Zealand on behalf of Council.

|

Content

Background

8 The Annual

Report 2015/2016 is in five sections. A summary of each is provided

below:

Section

1 - Overview

9 This contains

the overview of the Annual Report and includes:

· A

message from the Mayor and CE,

· A

description of the Annual Report,

· A

Shared Services Report,

· A

narration of the Executive Summary during the preceding year,

· A

Financial Overview which summarises Financial Performance, Financial Position

and the cash flows generated and applied by Council,

· Financial

benchmarks as per the Local Government Financial Prudence Regulations.

· Opportunities

for Māori to contribute to decision making,

· The

Audit Report (not included until the Annual Report is finalised),

· The

Statement of Compliance.

Section

2 - Council activities

10 Included

in here are details around Council’s main activities. It reports in

some detail on the achievement of the performance measures and provides a

summary of the funding received and applied in undertaking each activity.

It also includes details about key projects

under each activity group.

Section

3 - Council Controlled Organisations

11 This

section provides information around Council Controlled Organisations (Milford

Community Trust and the Southland Museum and Art Gallery).

Section

4 - Financial Information

12 This

section outlines Council’s accounting policies, financial statements and

notes to the financial statements.

Section

5 - other information

13 This

includes information about the Mayor and Councillors, the structure of Council,

Community Boards, other Subcommittees, the structure of the Executive

Leadership Team, and a glossary.

Status

of the Annual Report

14 At

the date of this report the Annual Report is substantially complete. The

principal matters outstanding include finalisation of the summary document, and

any final changes as a result of the final audit review processes.

15 Audit

New Zealand has completed the majority of its review of the Annual Report and

summary document and the final audit director review is now in progress.

This process may result in some changes to the document attached. Any

made will be outlined at the meeting.

16 As

with previous years, the summary document will be tabled and distributed at the

meeting on 28 September 2016.

Performance Measures

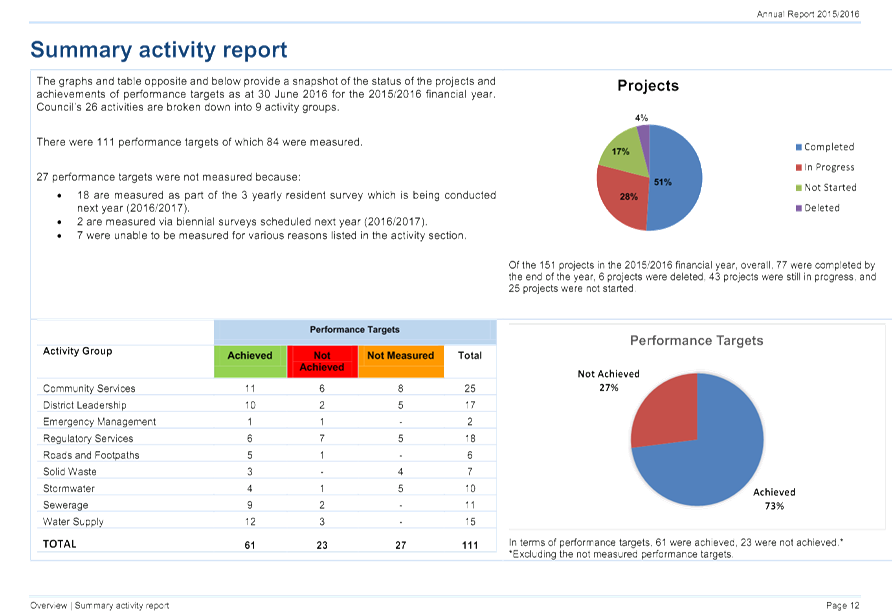

17 Council’s

26 activities are broken down into 9 activity groups each with their own

performance measures. There were 111 performance measures in total of which 86

were measured. Overall 61 were achieved and 23 were not achieved.

Financial

results

18 These

financial statements have been prepared in accordance with Tier 1 PBE

accounting standards.

19 Explanations

of the variance between actual results and budgeted results for 2015/2016 year

can be found in note 33 of the Annual Report (page 145).

20 A

summary of key financial information is set out below.

Statement of

Comprehensive Revenue and Expense (page 105)

21 The Statement of Revenue

and Expense records the revenue received and the expenditure incurred by

Council. It also records changes in the value of Council’s assets.

In summary, Council’s financial performance was as follows:

|

|

Actual 15/16

|

Budget 15/16

|

Actual 14/15

|

|

Total Revenue

|

$67.2M

|

$69.6M

|

$66.5M

|

|

Total Expenditure

|

($65.8M)

|

($67.1M)

|

($62.4M)

|

|

Operating

Surplus/(Deficit)

|

$1.4M

|

$2.5M

|

$4.1M

|

|

Gains on Assets at fair

value

|

$1.3M

|

-

|

$0.3M

|

|

Gains on Assets

|

$0.4M

|

$21.1M

|

($8.7M)

|

|

Total Comprehensive

Revenue and Expense

|

$3.1M

|

$23.6M

|

($4.3M)

|

22 Total

revenue was under budget primarily as a result of lower than budgeted NZTA

subsidy ($3.0M) and grants and subsidies, predominantly associated with AMCT

($1.8M). This was offset by increased forestry revenue ($1.4M) and

increased forestry revaluation ($1.2M).

23 Total

expenditure was under budget predominantly due to depreciation being $1.4M

lower than expected ($21.6M budget vs $20.2M). This was as a result of

the roading valuation at 30 June 2016 being significantly lower than expected

due to the reduction in bitumen prices

24 Gains

on Assets was also well under budget due to the significantly lower than

expected asset roading revaluation.

Statement of Financial Position (page 107)

25 The Statement

of Financial Position (also referred to as the Balance Sheet) records the

assets Council owns, and how those assets are financed. Total Assets is

what the council owns for example infrastructure assets, Total Liabilities are

finance from third parties, for example accounts payable, and Total Equity is the

net community assets (Total Assets less Total Liabilities). Key items in

the Statement of Financial Position were:

|

|

Actual 15/16

|

Budget 15/16

|

Actual 14/15

|

|

Total Assets

|

$1,400M

|

$1,478M

|

$1,398M

|

|

Total Liabilities

|

$11.0M

|

$12.2M

|

$11.7M

|

|

Total Equity

|

$1,389M

|

$1,466M

|

$1,386M

|

26 Total

Assets are significantly under budget primarily due to property, plant and

equipment being significantly less than budgeted by $85.1M. This is

primarily as a result of the lower than budgeted revaluation of infrastructural

assets and less capital works completed than anticipated.

Statement

of Cash Flows (page 108)

27 The

Statement of Cash Flows records the cash that Council received and

disbursed. Broadly cash, under financial reporting rules is recorded in

three separate categories:

• Operating

cash flows - the cash flow related to day-to-day operating activities.

• Investing

cash flows - the cash flow received from sale of assets and cash spent on

capital assets.

• Financing

cash flows - the cash flow received from any borrowings and the cash flow

disbursed in repaying borrowings.

28 Overall,

Council’s cash position decreased by $3.9M (rounded). In summary,

the cash flows recorded within these categories are as follows:

|

Operating cash flows

|

Actual 15/16

|

Budget 15/16

|

Actual 14/15

|

|

Cash surplus/(deficit)

|

$23.2M

|

$24.5M

|

$22.3M

|

|

Investing cash flows

|

Actual 15/16

|

Budget 15/16

|

Actual 14/15

|

|

Cash surplus/(deficit)

|

($27.1M)

|

($34.1M)

|

($24.2M)

|

|

Financing cash flows

|

Actual 15/16

|

Budget 15/16

|

Actual 14/15

|

|

Cash surplus/(deficit)

|

($0.01M)

|

($0.02M)

|

($0.02M)

|

29 Operating

cashflows were lower than budgeted. Income from NZTA reduced because

Council was able to undertake the same level of works at a reduced total cost

due to lower bitumen prices and a reduced programme. As funding from NZTA

is a percentage of dollars spent, the lower overall spend meant less income

received.

Issues

30 As

at the date of this report there are no unresolved issues in relation to the

Annual Report 2015/16. A small number of changes were requested by Audit

NZ and these have been made.

Factors to Consider

Legal

and Statutory Requirements

31 Section

98(1) of the Local Government Act 2002 requires the Council to prepare and

adopt an Annual Report each financial year. Section 98(4) requires

Council within one month after the adoption of the Annual Report to make

publicly available the Annual Report plus a summary of the information

contained in the Annual Report.

32 The

Annual Report reports on Council’s performance against the first year of

Council’s

10 Year Plan 2015-2025. The summary document summarises the key content

of the Annual Report.

33 Section

98(3) of the Local Government Act 2002 requires the Annual Report to be adopted

within four months of the end of the financial year to which it relates.

This makes 31 October the last day available to meet this timeframe.

Community

Views

34 As

the Annual Report is a report on activities undertaken during the year, no

consultation is required. Community views were considered as part of the

10 Year Plan 2015-2025 consultation process. This document outlines the

actual results compared to the budgeted results. The Annual Report and

summary document will be available to the public via Council’s website as

well as at Council offices.

Costs

and Funding

35 The

costs associated with the Annual Report include staff compilation time, audit

costs and printing and distribution costs. These costs are included in

the annual operating budgets and therefore not additional funding consideration

is necessary.

36 The

audit fee for the Annual Report 2015/2016 is $113,257 plus GST and

disbursements ($2,101 or 1.9% increase on 2014/2015 fee).

Policy

Implications

37 The Annual Report

2015/2016 reports to the public on Council’s performance against the

first year of Council’s 10 Year Plan 2015-2025.

Analysis

Options Considered

38 Under

the Local Government Act 2002, the Council must prepare and adopt an

Annual Report in respect of each financial year, no other options are

available.

Analysis of Options

Option

1- Adopt the Annual Report and associated summary document for the year ended

30 June 2016.

|

Advantages

|

Disadvantages

|

|

· Legal

compliance.

· The

document provides information to the public on the performance to budget and

against key performance indicators.

|

· There

are no disadvantages.

|

Option

2 - Do not adopt the Annual Report 2015/2016 and summary document.

|

Advantages

|

Disadvantages

|

|

· There

are no advantages of this option.

|

· Council

will not be compliant with the legislation.

|

Assessment

of Significance

39 The

Annual Report 2015/2016 is considered significant under Council’s

significance and engagement policy because the performance of Council is of

wide community interest.

40 It

is important to the public that Council meets both its financial and

non-financial commitments to ensure it delivers its services efficiently and

effectively. To do this the public relies on the information provided in

the Annual Report to give it assurance that Council is undertaking its

responsibilities and how well it is performing these.

41 Along

with the processes and procedures Council undertakes to track and record the

information provided in the Annual Report, to ensure that the public can rely

on the information provided an independent review is undertaken by auditors

(Audit New Zealand). In general the Audit New Zealand provides an

opinion as to whether Council has complied with Generally Accepted Accounting

Practice (GAAP) and that the annual report fairly reflects council’s

financial position, results of operations and cashflows, and levels of service

and reasons for any variance.

Recommended Option

42 The

recommendation is that the Council adopt the Annual Report and associated

summary document for the year ended 30 June 2016 (Option 1).

Next

Steps

43 Once

the Annual Report and summary document is adopted, and the signed

representation letter has been provided to Audit NZ (draft attached at appendix

C), the final audit opinion will be issued (draft attached at appendix

B). The audit opinion will be incorporated into the full and summary

annual report and an online and printed version will be made available to the

public.

Attachments

a Draft

Audit Opinion for the year ended 30 June 2016 ⇩

b Draft

Letter of Representation for the year ended 30 June 2016 ⇩

c Final

draft for adoption Annual Report 2015 2016 ⇩

|

Council

|

28 September 2016

|

|

Council

|

28 September 2016

|

|

Council

|

28 September 2016

|

|

Council

28 September

2016

|

|

Annual Plan Timetable 2017/2018

Record No: R/16/9/15556

Author: Katherine

McDonald, Corporate Planning and Performance Advisor

Approved by: Steve Ruru,

Chief Executive

☒

Decision ☐

Recommendation ☐

Information

Purpose

1 The

purpose of this report is to seek Council’s approval for the commencement

of work on the 2017/2018 Annual Plan and its associated timetable which is

indicative at this stage.

Executive

Summary

2 The

Local Government Act 2002 (LGA) Amendment Act 2014 introduced new requirements

around Annual Plans which have the effect of making the document much more

streamlined and focused on financial budgets.

3 Council

is asked to review and approve these process changes and the indicative

Annual Plan timetable.

|

Recommendation

That the Council:

a) Receives

the report titled “Annual Plan Timetable 2017/2018” dated 21

September 2016.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Agrees

the Annual Plan 2017/2018 is likely to include significant or

material differences from the content of the Long Term Plan 2015-2025

(LTP) and therefore Council intends undertaking public consultation before

adopting the plan in accordance with section 95 (2A) of the Local Government

Act 2002.

e) Approves

the indicative timetable for the preparation of the Annual Plan 2017/2018.

|

Content

Background

4 The

Local Government Act 2002 (LGA) Amendment Act 2014 introduced new requirements

around Annual Plans which have the effect of making the document much more

streamlined and focused on financial budgets.

5 Council

must still prepare and adopt an Annual Plan for each financial year.

6 The

purpose of an Annual Plan is to:

· Contain

the proposed annual budget and Funding Impact Statement.

· Identify

any variation from the financial statements and Funding Impact Statement

included in the 10 Year Plan in respect of the year.

· Provide

integrated decision making and co-ordination of the resources of the local

authority.

· Contribute

to the accountability of the local authority to the community.

7 Each

Annual Plan adopted must contain appropriate references to the 10 Year Plan and

set out the (financial) information required by Part 2 of Schedule 10 of the

Act which includes:

· Forecast

financial statements.

· Financial

statements for the previous financial year.

· Funding

Impact Statement (rating).

· Sample

properties.

· Rating

base information.

· Reserve

funds.

8 This

is a significant reduction in the level of requirements compared to what

Council has previously included in its Annual Plan and is likely to result in a

much smaller document.

9 Another

change as a result of the amendments is that there is no longer a requirement

to use the special consultation procedure and, if the Annual Plan does not

include significant or material differences from the content of the 10

Year Plan, then there is no requirement to consult.

10 The

intent of these legislative changes is to streamline annual planning processes

where possible so that greater effort can be made every three years around the

10 Year Plan.

11 The

more Council can align its planning cycles with this intent, the more it can

potentially gain benefits around efficiencies and focus its resources on

undertaking more effective community planning processes.

Issues

12 How

do the LGA requirements apply to Council’s 2017/2018 Annual Plan?

Consultation

13 If

Council prepares a document that follows the intent of the legislation it would

be an extremely streamlined document.

14 Section

95(2A) LGA provides that the requirement to consult as set out in Section 95(2)

“does not apply if the proposed Annual Plan does not include significant

or material differences from the content of the Long Term Plan for

the financial year to which the proposed Annual Plan relates”.

15 While

the test for significance is set under Council’s Significance and

Engagement Policy and requires a “major and long term effect” on

the District or community, the test for “materiality” is set much

lower. Materiality is defined in Section 95A(5) as follows:

16 “For

the purposes of this section, a difference, variation, or departure is material

if it could, itself or in conjunction with other differences, influence the

decisions or assessment of those reading or responding to the consultation

document”.

17 At

this stage it is highly likely that any variations to the budgets affecting

major projects or the cumulative effect of any carry-forwards will satisfy the

test. With the information we have, there are likely to be variations to the 10

Year Plan budgets for the Catlins Road sealing project, Around the Mountains

Cycle Trail and the Te Anau Wastewater Scheme. In addition, there could

be carry forwards for some projects.

18 Given

the low threshold for “materiality”, the indicative timetable has

been prepared on the basis that consultation will be required.

Local estimates process

19 In

addition to the amendments made to the 2016/2017 Annual Plan process, Council

is further considering its internal budgeting and local estimates processes for

the 2017/2018 Annual Plan. Historically, Council has allowed community

boards, CDAs and individual business units to re-open the 10 Year Plan budgets

on an annual basis. This has resulted in a complex process that occurs over a

number of months.

20 Council

staff are proposing a different process for the 2017/2018 Annual Plan as

follows:

21 Budgets

will be set at Year 3 of the 10 Year Plan, or updated estimates from the

2016/2017 Annual Plan where applicable. Budget managers will only be able to

request changes where the difference is significant (ideally +/- $10,000 but

will depend on the community and/or activity) and there is a good reason for

change.

22 Community

Engineers will be notified by email of their budgets and projects for Year 3,

and will be required to discuss any potential significant changes to projects

and/or budgets via informal workshops with their Community Boards (being held

in late October/early November). Any changes are to be notified to

Finance, and will be collated in a report to ELT for initial approval.

23 Community

Engineers will be required to discuss any potential significant changes to

projects and/or budgets via self-scheduled informal workshops with CDAs.

Any changes are to be notified to Finance, and will be collated in a report to

ELT for initial approval.

24 A

formal report will be included in the Community Boards and CDAs agenda for

approval at the meetings in late November/early December, confirming the final

budgets and the rates (no further changes will be made at these meetings).

25 Finance

staff will attend all Community Board workshops, but not inaugural meetings.

Finance staff will attend CDA estimate meetings only if there are key issues

for discussion.

26 District

rates setting and forecast financial statement preparation commences

immediately after the budgets close, resulting in the compilation of the draft

Annual Plan being available for adoption and consultation significantly earlier

than previous years.

27 Council

is asked to approve these new processes.

Annual Plan project and timetable

28 The

Project Manager for the 2017/2018 Annual Plan is Katherine McDonald, Corporate

Planning and Performance Advisor.

29 An

indicative timetable has been prepared based on the above assumptions and the

key milestones are as follows:

|

Annual Plan

Milestone (indicative)

|

Date

|

|

Community Boards

Workshops which include confirmation of budgets

|

17 October – 11

November 2016

|

|

CDA Inaugural Meetings

which include confirmation of budgets

|

21 November - 6 December

2016

|

|

Council workshop to

discuss draft Annual Plan

|

7 December 2016

|

|

Adoption of consultation

document

|

25 January 2017

|

|

Public consultation

|

20 February – 20

March 2017

|

|

Hearing of submissions

|

26-27 April 2017

|

|

Deliberation of

submissions

|

17 May 2017

|

|

Council workshop to

discuss final draft for feedback

|

Late May 2017

|

|

Adoption of Annual Plan

|

21 June 2017

|

30 Council

is asked to review and approve the timetable.

Factors to Consider

Legal

and Statutory Requirements

31 Pursuant

to section 95 of the LGA, Council is required to prepare and adopt an Annual

Plan for each financial year. Each Annual Plan must be adopted before the

commencement of the financial year to which it relates.

Community

Views

32 Council

is required in the course of its decision-making process to give consideration

to the views and preferences of persons likely to be affected by this

matter. Council should therefore consider the views of their community

boards and CDAs around the proposed budgeting processes.

Costs

and Funding

33 Producing

a streamlined version of the Annual Plan in accordance with the legislation and

streamlining the budgeting processes are likely to result in savings for the

organisation given the staff time that is normally dedicated to such

activities.

Policy

Implications

34 The

impact on the Annual Plan is outlined in this report.

Analysis

35 Options

Considered

1. Prepare

the Annual Plan as per the timetable (indicative).

2. Amend

the timetable with suggestions.

36 Analysis

of Options

Option 1 - Prepare

the Annual Plan as per the timetable (indicative).

|

Advantages

|

Disadvantages

|

|

· Staff

can proceed with the work required for the document as planned.

· Provides

a streamlined annual plan process.

|

· Nil

|

Option 2 - Amend the

timetable.

|

Advantages

|

Disadvantages

|

|

·

Nil

|

· Greater

administrative complexity.

|

Assessment of Significance

37 The

matter before Council is considered to have low significance.

Recommended

Option

38 Council

staff recommend Option 1 - Prepare the Annual Plan as per the timetable

(indicative).

39 Next Steps

40 Council

staff will communicate the changed process to staff and Community Boards and

CDAs. Council staff will progress with the preparation of the draft

Annual Plan.

Attachments

There are no attachments for

this report.

|

Council

28 September

2016

|

|

Mediation of the Appeals on the Proposed Southland

District Plan 2012 - Delegated Authority

Record No: R/16/9/14275

Author: Courtney

Ellison, Senior Resource Management Planner - Policy

Approved by: Bruce

Halligan, Group Manager Environmental Services

☒

Decision ☐

Recommendation ☐

Information

Purpose

1 To

grant delegated authority to the Team Leader - Resource Management to make

decisions on settling the remainder of the appeals to the Environment Court on

the Proposed Southland District Plan 2012, if possible through Environment

Court mediation.

Executive

Summary

2 Council

received nine appeals to the Proposed District Plan 2012, four of which have

been resolved through pre-mediation discussions with the appellants and

interested parties. In March 2015, delegation was granted to the Manager

Resource Management and Group Manager - Environment and Community to make

decisions on behalf of Council on the resolution of appeals. Changes in staff

and titles mean there is no longer a Manager - Resource Management, and

therefore this report seeks delegation be granted to the Team Leader - Resource

Management. The Group Manager - Environment and Community will continue to have

delegation under the resolution of Council on 18 March 2015.

|

Recommendation

That the Council:

a) Receives

the report titled “Mediation of the Appeals on the Proposed Southland

District Plan 2012 - Delegated Authority” dated 16 September 2016.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Grants

delegated authority to Team Leader - Resource Management to make decisions on

behalf of Council on appeals to the Proposed Southland District Plan 2012.

|

Content

Background

3 Appeals

on Resource Management Act decisions such as those made by the Resource

Management Committee on behalf of Council are subject to rights of appeal to

the Environment Court. Nine appeals were received on a relatively confined

number of topics out of 289 submissions and 48 further submissions made on the

Proposed Southland District Plan 2012.

4 Four

of these appeals have been settled as a result of staff discussions with the

appellants and interested parties and a consent order being lodged and

subsequently granted by the Environment Court.

5 The

remaining five appeals have not progressed as the Environment Court has put

these on hold until the Biodiversity section of the Proposed Southland Regional

Policy Statement (prepared by Environment Southland) has progressed. It is

anticipated that mediation on the Proposed Southland District Plan appeals

could progress late 2016 or in the first half of 2017.

Issues

6 Council

needs to be represented at the Environment Court mediation by people who have

the appropriate authority to settle appeals if an agreeable position is

reached.

7 On

18 March 2015 Council gave delegation to the Manager - Resource Management and

Group Manager - Environment and Community to make decisions on behalf of

Council in mediation on the Proposed Southland District Council 2012.

8 The

Manager - Resource Management position has recently been changed to a Team

Leader - Resource Management and therefore the delegation previously granted by

Council to the Manager - Resource Management is no longer valid. Therefore this

report is seeking delegation be granted to the Team Leader - Resource

Management.

Factors to Consider

Legal

and Statutory Requirements

9 In

order for Council to be appropriately represented at mediation in accordance

with the 2014 practice note issued by the Environment Court it needs to

delegate to a person or persons the authority to act on its behalf.

Community

Views

10 Community

views were sought through the submission process on the Proposed District Plan

and it is a small number of those people/organisations that have appealed the

decisions made to the Environment Court.

Costs

and Funding

11 Indicative

funding for this part of the plan making process has been included in the LTP

and annual plans for a number of years.

Policy

Implications

12 Any

settlement may affect the policy framework in the District Plan and not

entirely reflect the position that was initially reached in decisions by the

hearing panel.

Analysis

Options Considered

13 Council

must be represented in mediation proceedings and any subsequent Environment

Court hearing. Therefore the only option to consider is to whom the delegation

is made. It is considered that both the Team Leader – Resource Management

and the Group Manager – Environment & Community should have

delegation to ensure that someone is able to represent Council fully in

mediation if there are unforeseen circumstances. However, it is anticipated

that the Team Leader – Resource Management would be the primary

representative of Council.

Assessment of Significance

14 The

delegation of authority to settle appeals on the Proposed District Plan is not

a decision that will have a major or long term effect on an individual town or

the district, cultural impact, or level of service. Nor will it have a

financial impact that will exceed the threshold of 10% of total revenue

(exclusive of investment assets).

Recommended

Option

15 The

recommended option is to grant delegated authority to the Team Leader -

Resource Management to make decisions on behalf of Council.

Next

Steps

16 Staff

will attend Environment Court mediation on the outstanding appeals once

scheduled. The Resource Management Committee will be kept informed of progress

on the mediation process.

Attachments

There are no attachments for

this report.

|

Council

28 September

2016

|

|

Draft Reserves Management Policy

Record No: R/16/8/12517

Author: Kevin

McNaught, Strategic Manager Property

Approved by: Ian

Marshall, Group Manager Services and Assets

☒

Decision ☐

Recommendation ☐

Information

Purpose

1 This

report recommends the draft Reserves Management Policy for adoption by Council

including suggested amendments as a result of submissions.

Executive Summary

2 The

draft Reserves Management Policy was released for public consultation and one

submission was received. An amended draft policy reflecting feedback from the

submission is attached to this report and is recommended to Council for

adoption.

|

Recommendation

That the Council:

a) Receives

the report titled “Draft Reserves Management Policy” dated 16

September 2016.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Adopts

the attached draft of the Reserves Management Policy.

|

Content

Background

3 The

draft Reserves Management Policy was developed to provide a broad framework

that would apply to all reserves, parks and open spaces.

4 The

draft Reserves Management Policy would prevent the need for Council’s

broad approach to be duplicated in each of its Reserve Management Plans.

5 Council

released the draft Reserves Management Policy for public consultation and

received one submission.

Issues

6 The

submission received by Council (attached to this report) made a number of

suggestions which were discussed by officers.

7 Two

key amendments were made to the draft as a result of this submission. The draft

Reserves Management Policy (attached to this report) has included the

submitters wording relating to opportunity for an improvement in service

arising from leases and licences to occupy reserves.

8 Section

5.19 of the draft has also been amended to show that vegetation management will

occur in accordance with Reserve Management Plans.

9 Staff

have also suggested an amendment to include Council’s position on

election signs and hoardings. This is included in the attached draft in Section

5.17.

10 The

submission also raised a number of other points which have been addressed in

the table below:

|

Issue

|

Officer comments

|

|

Inclusion of a category of reserves for unformed

roads.

|

Officers did not agree that unformed road should be

classified as a class of reserve but considered that unformed road adjoining

a reserve could be managed along with the reserve as appropriate.

|

|

Clarification of policy relating to horses.

|

Officers recommend that this is dealt with through

Reserve Management Plans.

|

|

Inclusion of circus and fairground organisations.

|

Officers recommend that this is dealt with through the

provisions of the Trading in Public Places Bylaw 2013.

|

|

Inclusion of a policy statement relating to the

provision of playground equipment.

|

Officers did not support this suggestion, preferring a

community based approach to the provision of playground equipment depending

on the availability of funding and on community aspirations.

|

|

Specific criteria around the

design and size of signs.

|

This may be partially

addressed as part of ongoing work relating to Council branding.

|

Factors to Consider

Legal

and Statutory Requirements

11 Southland

District’s parks, reserves and open spaces are governed and regulated by

a broad range of legislation, plans, policies and bylaws. The Reserves Act 1977

applies to land that is a reserve subject to that Act.

12 The

draft Reserves Management Policy applies to all parks, reserves and open spaces

controlled by Southland District Council regardless of whether they are

classified as a reserve under the Reserves Act 1977. However, some specific

exemptions may be provided in individual Reserve Management Plans.

13 Under

Section 41 of the Reserves Act 1977, the Council is required to keep

Reserve Management Plans under continuous review. Since Reserve

Management Plans are aligned to the General Reserves Management Policy, this

policy will also be kept under continuous review.

14 As

well as aligning with other Southland District Council Plans and Policies, the

draft Reserves Management Policy also adheres to Environment Southland’s

Regional Plan and Ngāi Tahu ki Murihiku’s Natural Resource and

Environmental Iwi Management Plan 2008 - e Tangi a Tauira - The Cry of the

People.

15 The

draft Policy makes reference to a number of existing Southland District Council

bylaws. This ensures that the policy does not duplicate or contradict content

in existing regulatory instruments.

Community

Views

16 The

draft Reserves Management Policy was released for consultation under section 82

of the Local Government Act 2002, as it was not assessed as significant.

17 One

submission was received by Council. Council did, however receive a number of

verbal queries regarding individual Reserve Management Plans.

Costs

and Funding

18 There

are no funding issues associated with the implementation of the draft Reserves

Management Policy since the policy does not propose any significant changes in

the practice of reserve management. However, it does consolidate statements

about reserve management to prevent duplication of statements in Reserve

Management Plans.

Policy

Implications

19 The

draft Reserve Management Policy would enable the review of Reserve Management

Plans by providing a general policy framework that would not need to be

duplicated in each document.

20 The

draft Reserve Management Policy provides practical detail to support the

Southland District Council Open Spaces Strategy.

Analysis

Options Considered

21 Council

could:

· Option

1: Adopt the draft Reserves Management Policy with amendments to reflect

submissions;

· Option

2: Not adopt the draft Reserves Management Policy with amendments to reflect

submissions.

Analysis of Options

Option

1 – Adopt the draft Reserves Management Policy with amendments as

required

|

Advantages

|

Disadvantages

|

|

· The

draft Reserves Management Policy was supported by the submission received by

Council.

· Having

a broad framework for reserves management will prevent the need to duplicate

content in Reserve Management Plans. This will streamline the documents and

minimise the risk of inconsistency. It will also make the Reserve

Management Plans more user friendly and locally focused.

|

· No

significant disadvantages have been identified.

|

Option

2 – Not adopt the draft Reserves Management Policy with amendments to

reflect submissions

|

Advantages

|

Disadvantages

|

|

· No

significant disadvantages to this approach.

|

· If

Council did not adopt a Reserve Management Policy the approach would need to

be articulated in each Reserve Management Plan. This could lead to

inconsistency and would make Reserve Management Plans less succinct.

|

Assessment of Significance

22 The

draft Reserves Management Policy has not been assessed as significant. It does

not propose substantial changes to the way in which Council would approach

reserve management, nor does it impose significant restrictions on reserve

users. The policy does however, clarify a proposed position on a number of

issues and refer to a number of existing bylaws.

Recommended

Option

23 It

is recommended that the Council adopt the draft Reserves Management Policy with

any amendments as required (Option 1).

Next

Steps

24 The

adoption of the draft Reserves Management Policy would allow Council officers

to commence a gradual review of Reserve Management Plans. This would involve

engagement with local communities.

Attachments

a Submission

- Draft Reserves Management Policy ⇩

b Draft

Reserves Management Policy ⇩

|

Council

|

28 September 2016

|

Graham Jones

Draft

Reserves Policy Submission

I support the overall

approach of the draft policy. However, to provide better clarity for all

users, I submit that the following additions should be considered:

4.0 Background

Consider adding a third

type of land treated as reserve – that of unformed road. An example

is the Pearl Harbour road line on the Manapouri Foreshore which is incorporated

under that management plan.

5.5 Leases & Licences

to Occupy

Suggest amend wording to:

Council may enter in agreements when there is a clear requirement for

consistent use or service or a demonstrated opportunity for reliable

improvement in service. The purpose of this suggested amendment is to

leave opportunity open for entrepreneurs who wish to develop new compatible

businesses such as a tea kiosk on a reserve but there is no past history of

such usage.

5.6 Animals

For the sake of clarity

include a specific policy relating to the riding for horses on reserves.

I believe that the detailed text of other council reference documents is in

conflict with itself – both allowing and disallowing the riding of

horses.

5.9 Trading

Consider whether use of

reserves by itinerant circus and fairground organisations warrants specific

mention.

5.15 Play Equipment

Suggest extend this

section to include actual policy on the provision or non-provision of

playgrounds, perhaps treated on a district wide basis, the same as toilets in

sec 5.14.

5.16 Signs and

Interpretation

Include policy for the

physical provision of signage, including aspects such as size, style,

symbology, colours or a reference to a design document.

5.19 Landscaping and

Vegetation

Include a policy allowing

for Council contractors to maintain vegetation, including trimming and removal

of unsightly, diseased, rotten or dangerous tree limbs or trees or those

causing excessive shading, root damage or loss of amenity views. The

existing wording is strongly aimed at the retention of native vegetation, which

is good, but experience on the Manapouri Foreshore reserve shows that a balance

is needed.

I acknowledge that good

policy needs to be kept as broad as possible to cover all possible situations

arising. However my suggestions for more specific inclusion are aimed at

improving the usability of the document both for the guidance of council

officers who have to administer the policy and for ratepayers who wish to

undertake activities on reserves.

Graham Jones

13 June 2016

|

Council

|

28 September 2016

|

SOUTHLAND DISTRICT COUNCIL

RESERVES MANAGEMENT POLICY

DOCUMENT CONTROL

|

Policy Administrator:

Strategic Manager Property

|

TRIM reference number:

|

Effective date:

|

|

Approved by:

Council

|

Date approved:

|

Next review date:

|

Contents

1.0 PURPOSE.. 1

2.0 SCOPE.. 1

3.0 DEFINITIONS.. 1

4.0 BACKGROUND.. 1

4.1 The Reserves

Act 3

4.2 Local Context 3

5.0 POLICY

STATEMENTS.. 3

5.1 Council

Approval 3

5.2 General Access. 3

5.3 Pedestrian

Access. 3

5.4 Vehicle Access. 4

5.5 Leases and

Licences to Occupy. 4

5.6 Animals. 4

5.7 Aircraft and

Helicopter Landings. 4

5.8 Sale and

Consumption of Alcohol 4

5.9 Trading. 5

5.10 Fires. 5

5.11 Fireworks Displays. 5

5.12 Buildings and Structures. 5

5.13 Boundaries and Fencing. 6

5.14 Toilets. 6

5.15 Play Equipment 6

5.16 Signs and Interpretation.. 6

5.17 Electoral advertisements and

hoardings. 6

5.18 Pest Plant and Pest Animal Control 6

5.19 Litter Control and Dumping. 6

5.20 Landscaping, Amenity Planting

and Areas of Native Vegetation.. 7

5.21 Memorials. 7

5.22 Monuments, Artwork and Sculptures. 7

5.23 Outdoor Furniture. 7

5.24 Network Utility Infrastructure. 7

5.25 Lighting. 7

6.0 ROLES AND

RESPONSIBILITIES.. 9

7.0 ASSOCIATED

DOCUMENTS.. 9

8.0 REFERENCES.. 10

9.0 REVISION

RECORD.. 10

|

Council

|

28 September 2016

|

1.0 PURPOSE

This

policy provides guidance on the administration, use, maintenance and

development of reserves across the Southland District.

2.0 SCOPE

Policy

statements in this document apply to all parks, reserves and open spaces

controlled by Southland District Council unless specific exemption is provided

in individual Reserve Management Plans.

3.0 DEFINITIONS

|

Term

|

Meaning

|

|

Activity Management Plan (AMP)

|

The Parks and Reserves Activity Management Plan is

used to document Council’s management practices for parks and reserves

over a 30 year period.

|

|

Council/the Council

|

Southland District Council as the land owner/

administering body of reserves.

|

|

Long Term Plan (LTP)

|

Southland District Council’s Long Term

Plan. It is also referred to as the 10 Year Plan.

|

|

Parks, Reserves and Open Spaces

|

The term reserve refers to any parcel of land owned,

administered and/or managed by Council, as a reserve, park, or open space.

|

|

Reserve Management Plan

|

Reserve Management Plans are a requirement of

Section 41 of the Reserves Management Act 1977. Reserve Management

Plans provide direction for the day-to-day management of reserves and details

about factors that impact upon reserves. They also establish clear directions

for future management and development.

|

|

Unmanned Aerial Vehicles/ UAVs

|

The term Unmanned Aerial Vehicle (UAV) is defined in

the Southland District Council Unmanned Aerial Vehicles Policy. The

term UAV covers all electric powered remote controlled model aircraft,

including the type commonly referred to as ‘drones’ that are

capable of vertical take-off and landing and small hand-launched gliders with

less than a 1.5 metre wing span.

|

4.0 BACKGROUND

Southland District has

155 reserves, parks and open spaces, distributed over a land area of

30,400.94 km². Southland District’s reserves offer an

extensive range of recreational opportunities and environmental

characteristics.

Reserves owned, administered and/or managed by the Council

have two distinct forms of legal status:

• land

held subject to the Reserves Act 1977, and classified according to its

principal purpose

• freehold

land held by Council in fee simple title for parks purposes but not held under

the Reserves Act.

The Reserves Act 1977 applies to all public land that has

been vested or gazetted under the Act and specifies in general terms the

purpose of each class of reserve. The Act also requires that each reserve

be managed in accordance with its purpose and classification.

The terms parks, reserves and open spaces could also refer

to parcels of land held by the Council for a wide variety of purposes akin to

those described in the Reserves Act or the Local Government Act 2002.

Not all of these parcels of land are protected under these Acts.

Southland

District’s parks, reserves and open spaces are governed and regulated by

a broad range of legislation, plans, policies and bylaws.

4.1 The

Reserves Act

The

Reserves Act 1977 applies to land that is gazetted as a reserve under the

Act. While the term park(s) is used in this document, not all parks are

reserves under the Reserves Act 1977. The management of these parks,

however, will not differ in general terms from reserves as defined by the

Reserves Act 1977.

Under Section 41 of the

Reserves Act 1977, the Council is required to keep Reserve Management

Plans under continuous review. Since Reserve Management Plans are aligned

to the General Reserves Management Policy, this policy will also be kept under

continuous review.

4.2 Local

Context

As

well as aligning with other Southland District Council Plans and Policies, the

General Reserves Management Policy also adheres to Environment

Southland’s Regional Plan and Ngāi Tahu ki Murihiku’s Natural

Resource and Environmental Iwi Management Plan 2008 - e Tangi a Tauira - The

Cry of the People.

5.0 POLICY STATEMENTS

5.1 Council

Approval

Some activities outlined in this

policy require specific approval or authorisation from the Council. The

nature and context of the activity will determine how approval may be

granted. For further information on how to obtain approval for specific

activities, please contact Southland District Council.

5.2 General Access

Unless

it is limited by the Reserves Act 1977, public access to reserves is a

right.

The Council provides a level and standard of access to reserves that is

appropriate to how each reserve is used.

Several

factors may impact on public access to reserves. These include:

•

leases or licences to occupy the reserve

held by third parties

•

safety issues

•

activities that are

occurring on a reserve for a period of time (eg planting or construction) or

•

other restrictions under the Reserves Act

1977.

Clubs and organisations may gain

exclusive use of a reserve for a specific period of time (eg during organised

sports teams training or match occasions) with prior written approval from the

Council.

From

time to time, reserves may be closed to the public and a rental charged for the

entry by an organisation staging a special event. This is subject to

Section 53(1)(e) of the Reserves Act 1977 and requires the written approval of

the Council.

5.3 Pedestrian

Access

If required, pedestrian access

will be controlled by the provision of walking tracks, footpaths and

footbridges.

Where

practical, access to reserves and reserve facilities will be inclusive and will

consider universal design. Walking tracks will be maintained to the

appropriate standard developed by the Department of Conservation and Standards

New Zealand

as set out in the “New Zealand Handbook - Tracks and Outdoor Visitor

Structures (SNZ HB 8630:2004)”.

5.4 Vehicle

Access

Council

may provide access roads and parking facilities within reserves.

Motorised vehicles, other than maintenance vehicles, must only be used on

roadways or parking areas unless prior written approval from the Council has

been obtained.

Use

of non-motorised vehicles (such as bicycles, skateboards and roller-blades) is

permitted provided their use does not endanger other reserve users, cause

damage to the reserve or make undue noise.

Non-motorised

vehicles should not be used on walking tracks unless there is a sign indicating

that their use is permitted.

5.5 Leases and Licences to Occupy

The

Council may enter into formal lease agreements on reserve land when the land is

available and there is a clear requirement for consistent use or service or a demonstrated opportunity for reliable improvement in

service. Management responsibilities of the lessee will be clearly

identified in the lease agreement.

5.6 Animals

Dog

access to parks and reserves is determined by Southland District Council’s

Dog Control Bylaw 2015. The Dog Control Bylaw 2015 also

determines what degree of control is required on reserves where dogs are

allowed.

Signage

or information in the Reserve Management Plans will indicate if other animals

are specifically excluded on any reserve.

Council

may use grazing as a management tool on reserves. Grazing will comply

with the Southland District Council Roading Bylaw and the Southland District

Council Keeping of Animals, Poultry and Bees Bylaw.

5.7 Aircraft and Helicopter Landings

Landing

an aeroplane, helicopter or any kind of flying machine in a Council reserve is

not permitted without prior written approval from the Council.

Emergencies are an exception to

this rule. Parties wishing to use any reserve for the purpose of landings

during special events or for approved training exercises should contact

Southland District Council for further advice.

5.8 Sale and Consumption of Alcohol

Consumption

of alcohol in public spaces is regulated by legislation and the

Alcohol Control Bylaw. The sale and supply of alcohol is regulated

by the Sale and Supply of Alcohol Act 2012. Council permits special

licences to be issued for the sale and supply of alcohol on reserves.

Club licences may be issued to lease holders within reserves.

5.9 Trading

Trading

in reserves must comply with Section 54 (1) (d) of the Reserves Act 1977 and

may be subject to the Trading in Public Places Bylaw.

Section 54 (1) (d) of the

Reserves Management Act 1977 allows trading to occur under leases and licences

or for a temporary occupation of not more than six consecutive days.

Trading activities must be necessary to enable the public to obtain the benefit

and enjoyment of the reserve or for the convenience of persons using the

reserve.

Applications to trade in reserves

for a period of not more than six consecutive days will be administered under

the Trading in Public Places Bylaw. Applications to trade in reserves for

a longer time period will require a lease or licence. If trading is

contemplated under the relevant Reserve Management Plan, applications will not

be publicly notified. If trading is not contemplated under the relevant

Reserve Management Plan, applications will be publicly notified and an

opportunity for objections will be provided.

When making decisions regarding

applications to trade on reserves, Council will consider a number of factors

including the nature of trading, its impact on other reserve users and the

effect on the reserve and existing infrastructure and facilities.

5.10 Fires

Lighting

fires outside of a contained barbecue is not permitted on reserves unless there

is prior written approval from the Council and the Southern Rural Fire

Authority.

5.11 Fireworks Displays

Fireworks

displays must:

•

be approved by the local

community board, community development area subcommittee or Council

•

be undertaken only by people authorised by

Council

•

have a safety plan

(including fire control) that has been approved by the Council

•

have any approvals

required under the Hazardous Substances and New Organisms Act

•

have a fire permit

issued by the Southern Rural Fire Authority if the display is during a

Restricted Fire Season.

5.12 Buildings and Structures

The

number of buildings and structures on reserves will be limited to a level that

facilitates the safe and appropriate use of each reserve. Sharing

facilities by more than one club or group is encouraged.

All

new buildings or major changes to existing buildings and structures on reserves

require approval from Council as the land owner of the reserve. Council

will consider how buildings and structures will integrate with the natural environment

of the reserve. The Building Act 2004 and the Southland District Plan may

also include other requirements which must be met.

Buildings

and structures will be maintained to a high standard and, where practical,

designed to limit the opportunity for vandalism.

5.13 Boundaries and Fencing

The

Council will reach an agreement with adjoining land owners on the type and

standard of fencing and the contributions made by each party. On

occasion, fencing may not be required. Required contributions may be

financial or made through the provision of materials or labour.

There may be some situations

where Council is not required to contribute to a boundary fence, for example if

there is an existing fencing covenant.

Consideration

will be given to the needs of the Council and the adjoining land owner.

The characteristics of the reserve and the land use of adjoining neighbours

will also influence Council’s decisions in relating to fencing.

Decisions relating to fencing will be formalised through a fencing

agreement.

Where it is impractical or

undesirable to erect a fence on a reserve boundary, the fence may deviate from

the legal boundary with the agreement of the adjoining land owner.

5.14 Toilets

A

district-wide approach is taken to the number, location and standard of public

toilets. Proposals for new toilets are considered against criteria which

take into consideration requirements and availability across the

District.

5.15 Play Equipment

All

new playgrounds and replacement of playground equipment will comply with the

Building Act 1991, the Resource Management Act 1991 and the New Zealand

Safety Standards NZS 5828:2004 or subsequent updates.

The

design and location of each playground will reflect the visual character of the

reserve and consider environmental factors such as the orientation of the sun,

shelter from the wind, visibility and disturbance to adjoining properties.

5.16 Signs and Interpretation

The

placement of signs on reserves by non-Council organisations requires written

approval from Council. Advertising signs are subject to the Southland

District Plan.

Council will ensure that new or

replacement signage identifies places that are of cultural significance in

accordance with the Ngāi Tahu Claims Settlement Act 1998.

5.17 Electoral advertisements and hoardings

No

election hoardings and signs are permitted to be placed or erected in Council

controlled or owned parks, reserves and open spaces.

5.18 Pest Plant and Pest Animal Control

Pest

plants and animals on Council reserves will be controlled in accordance with

Environment Southland’s Regional Pest Management Strategy.

5.19 Litter Control and Dumping

Litter

bins may be provided on reserves at strategic locations and in sufficient

numbers to meet the reasonable demands of the users. These bins will be

cleared regularly to prevent overfill and spillage.

Where

there are no litter bins, reserve users are required to remove all litter from

the reserve. The dumping of refuse including garden waste on reserves is

an offence under the Litter Act 1979.

5.20 Landscaping, Amenity Planting and Areas of Native

Vegetation

Landscaping

and amenity planting and vegetation management

will be undertaken on reserves in accordance with Reserves Management Plans.

Any

new plantings on a reserve will consider visibility and safety. The

retention of indigenous vegetation and threatened plants on reserves is a

priority for the Council. Where possible, existing native vegetation on

reserves shall be preserved and revegetated using locally sourced native

species. The use of exotic species will be restricted to areas where

exotic species predominate and/or the recreational use of the reserve would be

enhanced by the use of exotics (eg for shade).

The

removal or damage to any tree, shrub or plant material from within reserves is

prohibited without the prior written approval of the Council.

5.21 Memorials

Memorials

and plaques for individuals are only permitted in locations identified in

Reserve Management Plans. All memorial plantings and commemorative

plaques require written approval from the Council.

5.22 Monuments, Artwork and Sculptures

Monuments,

art work and sculptures must have relevance to the reserve and enhance the natural

surroundings. When determining whether the placement of a monument,

artwork or sculpture is appropriate, the nature of the item, the proposed

location, reserve use and reserve values will be considered.

Maintenance

of monuments, artworks and sculptures will be undertaken by Council staff, or

contractors, unless agreed otherwise at time of construction.

5.23 Outdoor Furniture

Outdoor

furniture will be appropriate to the needs of reserve users. The nature

of outdoor furniture, including materials and colour will be consistent with

the natural surroundings. All outdoor furniture will be approved by the

Council.

Maintenance

of outdoor furniture will be undertaken by the Council staff or contractors.

5.24 Network Utility Infrastructure

Reserves

are often crossed by network utility infrastructure, particularly power

pylons. While most of these have been in place for many years, the

Council will only consider new requests to place utility infrastructure in a

reserve if all alternative options have been considered.

5.25 Lighting

Lighting

may be provided for walkways and parking areas in reserves. Impacts on

adjoining land owners are considered in relation to ground lighting or lighting

outside buildings.

Where

there are sports grounds in a reserve, lighting for night time training may be

considered. Controls on lighting usage may be imposed by the

Council.

6.0 ROLES AND RESPONSIBILITIES

Reserve users are responsible for

ensuring that their use, activity, or any associated buildings or structures

comply with relevant legislation, the Southland District Plan, Southland

District Council Policies and Council Bylaws.

Some other documents which

regulate activity on reserves are provided in the table below.

|

Activity

|

Regulated by

|

|

Camping

|

Freedom Camping Bylaw

|

|

Consumption of alcohol

in public places

|

Alcohol Control Bylaw

and Summary Offences

|

|

Sale and supply of

alcohol

|

Sale and supply of

Alcohol Act 2012

|

|

Dogs

|

Dog Control Bylaw and

Dog Control Act 1996

|

|

Other animals

|

Keeping of Animals,

Poultry and Bees Bylaw

|

|

Trading

|

Trading in Public Places

Bylaw

|

|

Unmanned aerial vehicles

|

Unmanned Aerial Vehicle

Policy

|

7.0 ASSOCIATED DOCUMENTS

This

document should be considered in the context of the following associated

documents:

Bylaws:

• Southland

District Council Dog Control Bylaw

• Southland

District Council Keeping of Animals, Poultry and Bees Bylaw

• Southland

District Council Alcohol Control Bylaw

• Southland

District Council Trading in Public Places Bylaw

• Southland

District Council Animal Management Bylaw

• Southland

District Council Freedom Camping Bylaw

• Southland

District Council Roading Bylaw

Plans:

• Reserve

Management Plans

• Southland

District Plan

• Southland

District Council Long Term Plan

• Parks

and Reserves Activity Management Plan

•

Southland District Council Animal Management Bylaw

Strategy:

•

Southland District Council Open Spaces Strategy

Policies:

• Southland

District Council Unmanned Aerial Vehicles Policy

•

Southland District Council Smoke Free Open Spaces

Policy

Acts:

• Reserves

Act 1977

• Resource

Management Act 1991

• Local

Government Act 2002

• Sale

and Supply of Alcohol Act 2012

• Building

Act 2004

• Health

Act 1956

•

Fencing Act 1978

8.0 REFERENCES

• New

Zealand Handbook - Tracks and Outdoor Visitor Structures

(SNZ HB 8630:2004)

• New Zealand

Safety Standards NZS 5828:2004

9.0 REVISION

RECORD

|

Date

|

Version

|

Revision Description

|

|

«Type

Date»

|

«Version»

|

«Revision»

|

|

«Type

Date»

|

«Version»

|

«Revision»

|

|

«Type

Date»

|

«Version»

|

«Revision»

|

|

Council

28 September

2016

|

|

Council

Interest in Land Delegation

Record No: R/16/9/14792

Author: Kevin

McNaught, Strategic Manager Property

Approved by: Steve Ruru,

Chief Executive

☒

Decision ☐

Recommendation ☐

Information

Background

1 With

property information becoming more accessible, a consequence is that more

issues are being identified, which require a resolution.

2 This

is primarily related to owners and occupiers of private property becoming aware

that some portions of land are either unknown or are not in their ownership.

Officers have, for example, recently looked at an issue relating to a section

of private farm land on which a section was identified for road but was never

formally designated as such. There are processes available to rectify this type

of anomaly. However, these processes are becoming more complex and regularly

require the input of Council to the extent that it can either make a claim (or

not) to the land.

3 The

processes being required by LINZ and others to address these issues are now

requiring statements and/or declarations to that effect, and the officers

dealing with these are required to state that they are duly authorised by the

Southland District Council to make the statement or declaration.

4 Historically,

this has not been required nor been an issue, however to make these specific

statements or declarations a delegation from Council is required.

5 This

is a normal operational issue that officers will either receive or do the

relevant research and form an opinion as to whether Council has an interest or

not in the land. This delegation is required as a result of the changing

processes to complete all the relevant documentation to rectify the anomalies.

|

Recommendation

That the Council:

a) Receives

the report titled “Council Interest in Land Delegation” dated 9

September 2016.

b) Delegates

to the Chief Executive and the Group Manager Services and Assets authority to