Notice is hereby given that a Meeting of

the Activities Performance Audit Committee will be held on:

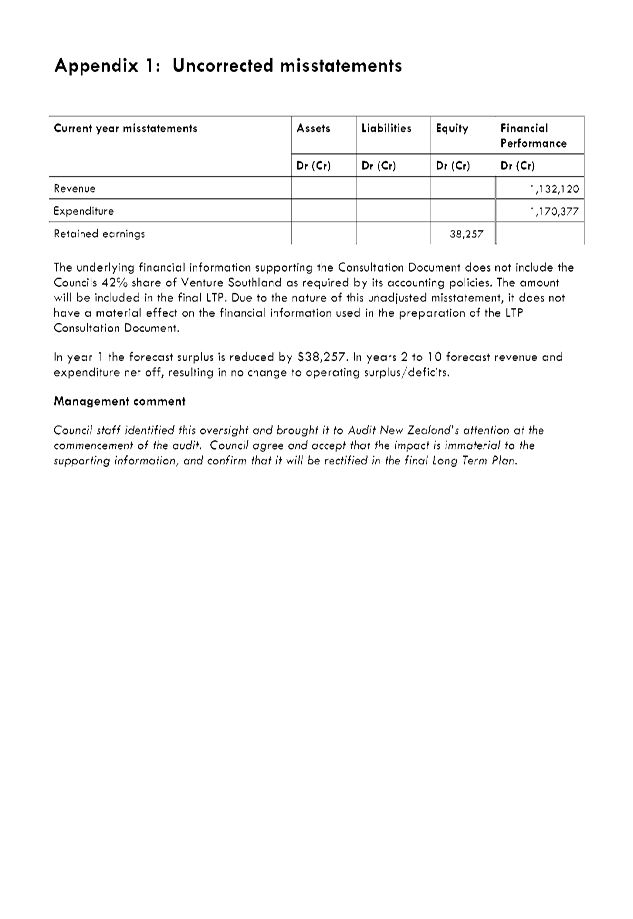

|

Date:

Time:

Meeting Room:

Venue:

|

Wednesday, 3

June 2015

10.30am

Council Chambers

15 Forth Street

Invercargill

|

|

Activities Performance Audit Committee Agenda

OPEN

|

MEMBERSHIP

|

Chairperson

|

Councillor Lyall Bailey

|

|

|

|

Mayor Gary Tong

|

|

|

Councillors

|

Councillor Stuart Baird

|

|

|

|

Councillor Brian Dillon

|

|

|

|

Councillor Rodney Dobson

|

|

|

|

Councillor John Douglas

|

|

|

|

Councillor Paul Duffy

|

|

|

|

Councillor Bruce Ford

|

|

|

|

Councillor George Harpur

|

|

|

|

Councillor Julie Keast

|

|

|

|

Councillor Ebel Kremer

|

|

|

|

Councillor Gavin Macpherson

|

|

|

|

Councillor Neil Paterson

|

|

IN ATTENDANCE

|

Chief Executive

|

Steve Ruru

|

|

|

Committee Advisor

|

Fiona Dunlop

|

|

Terms of

Reference for the Activities Performance Audit Committee

This committee is a committee of Southland

District Council and has responsibility to:

·

Monitor and review Council’s performance

against the 10 Year Plan

·

Examine, review and recommend changes relating

to Council’s Levels of Services.

·

Monitor and review Council’s financial

ability to deliver its plans,

·

Monitor and review Council’s risk

management policy, systems and reporting measures

·

Monitor the return on all Council’s

investments

·

Monitor and track Council contracts and

compliance with contractual specifications

·

Review and recommend policies on rating, loans,

funding and purchasing.

·

Review and recommend policy on and to monitor

the performance of any Council Controlled Trading Organisations and Council

Controlled Organisations

·

Review arrangements for the annual external

audit

·

Review and recommend to Council the completed

financial statements be approved

·

Approve contracts for work, services or supplies

in excess of $200,000.

|

Activities Performance Audit Committee

03 June 2015

|

|

TABLE OF

CONTENTS

ITEM PAGE

Procedural

1 Apologies 5

2 Leave of

absence 5

3 Conflict of

Interest 5

4 Public Forum 5

5 Extraordinary/Urgent

Items 5

6 Confirmation

of Minutes 5

Reports for Resolution

7.1 Financial

Report to 31 March 2015 7

7.2 Report

to Activities Performance Audit Committee on outcome of 2015 International

Accreditation New Zealand (IANZ) Reaccreditation Audit of Southland District

Council Building Control Section 39

7.3 Request

for Council to Maintain Irthing Road, Five Rivers 49

7.4 Signs

Maintenance Service 59

Reports for Recommendation

8.1 Southland

District Council 2015/2016 Resurfacing Contract - Contract 15/21 61

8.2 Health

and Safety 65

8.3 Management

Report from Audit New Zealand for the 2015-25 Consultation Document 69

8.4 Council's

Insurance Policies 83

8.5 Venture

Southland - Relationship Management and Approach 93

Public Excluded

Procedural motion

to exclude the public 99

C9.1 Public

Excluded Minutes of the Activities Performance Audit Committee Meeting dated 22

April 2015 99

C9.2 Milford

Development Authority Update 99

C9.3 Professional

Services Contract 12/03 Extension 99

At the close of

the agenda no apologies had been received.

2 Leave

of absence

At the close of

the agenda no requests for leave of absence had been received.

3 Conflict

of Interest

Councillors are

reminded of the need to be vigilant to stand aside from decision-making when a

conflict arises between their role as a councillor and any private or other

external interest they might have. It is also considered best practice for

those members in the Executive Team attending the meeting to also signal any

conflicts that they may have with an item before Council.

4 Public Forum

Notification to

speak is required by 5pm at least two days before the meeting. Further

information is available on www.southlanddc.govt.nz

or phoning 0800 732 732.

5 Extraordinary/Urgent

Items

To consider, and if

thought fit, to pass a resolution to permit the Council to consider any further

items which do not appear on the Agenda of this meeting and/or the meeting to

be held with the public excluded.

Such resolution is

required to be made pursuant to Section 46A(7) of the Local Government Official

Information and Meetings Act 1987, and the Chairperson must advise:

(i) The

reason why the item was not on the Agenda, and

(ii) The

reason why the discussion of this item cannot be delayed until a subsequent

meeting.

Section 46A(7A) of the Local Government Official Information and Meetings

Act 1987 (as amended) states:

“Where an item

is not on the agenda for a meeting,-

(a)

That item may be discussed at that meeting if-

(i)

That item is a minor matter relating to the general

business of the local authority; and

(ii)

the presiding member explains at the beginning of the

meeting, at a time when it is open to the public, that the item will be

discussed at the meeting; but

(b)

no resolution, decision or recommendation may be made in

respect of that item except to refer that item to a subsequent meeting of the

local authority for further discussion.”

6 Confirmation

of Minutes

6.1 Meeting minutes of Activities Performance

Audit Committee, 13 May 2015

|

Activities

Performance Audit Committee

03 June 2015

|

|

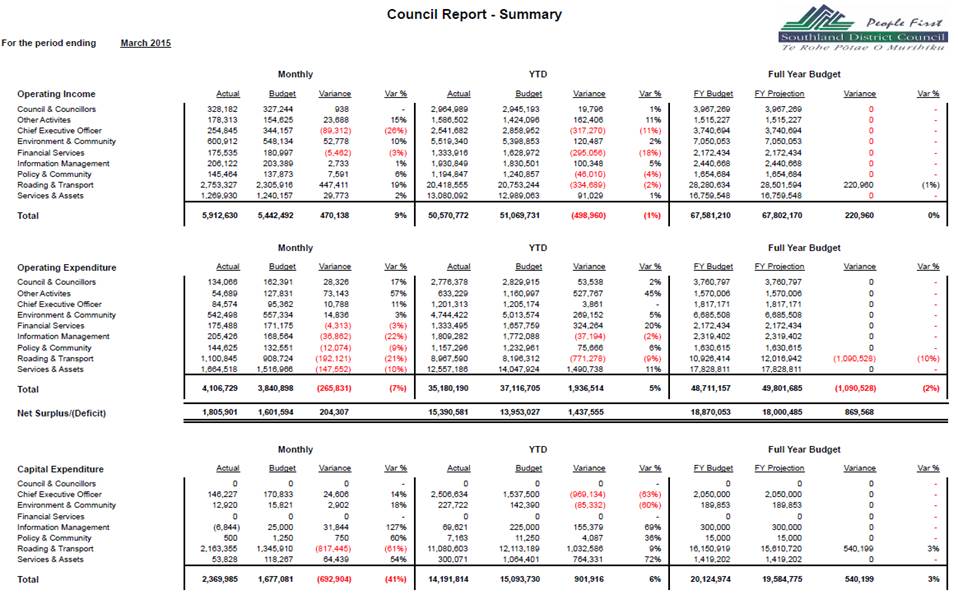

Financial

Report to 31 March 2015

Record No: R/15/4/7341

Author: Susan McNamara, Management Accountant

Approved by: Anne Robson, Chief Financial Officer

☐

Decision ☐ Recommendation ☒ Information

|

Recommendation

That the Activities Performance Audit Committee:

a) Receives

the report titled “Financial Report to 31 March 2015” dated 18

May 2015.

|

Attachments

a Report to Activities

Performance Audit Committee - 3 June 2015 - Financial Report to 31 March 2015 View

|

Activities

Performance Audit Committee

|

03 June 2015

|

Background

This report outlines the financial results to 31 March

2015.

Percentage of year gone: 75%.

OVERVIEW

Management Accountant March Finance Overview

As in prior years, all budget managers have been instructed

to have a strong focus on their budget and expenditure items.

The financial commentary centres on the summary sheet which

draws the totals from each of the key sections together. Although you are

able to obtain more detailed key variance explanations from senior managers in

these sections, these will be summarised below, concentrating on the YTD

results.

Income

Overall for the YTD, income is 1% ($499K) under budget

Key variances are as follows:

The Council and Councillors’ activity is 1% ($20K)

over budget for the year-to-date. This is the result of on charging other

departments for catering ($13K) and the recovery of costs relating to the

demolition of a dangerous building ($7K).

Other activities’ income is 11% ($162K) over budget

for the year-to-date.

This is predominantly due to the timing of income received from interest on

investments.

Within the Chief Executive section, income received is $317K

(11%) under budget due to:

• Chief

Executive - Income is $27K (6%) over budget due to proceeds from an unbudgeted

vehicle sale and rates penalties.

• Stewart

Island Visitors Levy - $16K (13%) under budget. With the cruise ship

period completed, income is expected to be well under budget at year end.

• Around

the Mountains Cycle Trail - $384K (26%) under budget due to substantial

invoicing to the Ministry being completed last financial year.

Within the Environmental and Community Group, year-to-date

income is $120K (2%) over budget; this is principally due to increased revenue

in Dog and Animal Control from increased numbers of dog registrations $18K and

infringement notices $57K.

Within the Financial Services Group, income is $295K (18%)

under budget. As this activity is internally funded, this is a result of

reduced expenditure.

Within the Information Management Group, year-to-date income

is $100K (5%) over budget, predominantly due to internal photocopying charges

$34K (forecast to be $17K over at year end) and internal computer hire $29K

(forecast to be $37K over at year end).

Within the Policy and Community Group, year-to-date income

is $46K (4%) under budget. As this activity is internally funded this is a

result of reduced expenditure primarily on staff costs.

Within the Roading and Transport section, income is 2%

($335K) under budget; this is expected to align slightly before year end with a

projection of $221K under budget by then.

Overall Services and Assets income

(excluding roading) is tracking $91K (1%) above

year-to-date budget. This is due to:

• Overall

Forestry income received is $108K (6%) over budget. This is expected to

be the position at year end.

• District

Water is $19K (1%) over budget due to unbudgeted water tanker charges ($3K),

water connection fees ($2K), increased water meter income ($6K) along with

rates adjustments ($5K)

• District

Sewerage is $16K (1%) over budget due to unbudgeted sewerage connection fees

($5K) along with rates adjustments ($11K)

• Waste

Management is $16K (1%) over budget due to a difference between the phasing of

the budget for the Waste Minimisation Levy and when the income has been

received. Income is expected to realign with the budget at the end of the

year.

• District Reserves is $14K under budget as some reserve

transfers for Curio Bay have yet to be actioned.

• Engineering Consultants is $57K (9%) under budget. As

income is fully recovered and driven by

expenditure levels the reduced expenditure impacts directly on

income.

Expenditure

Overall for the year-to-date, expenditure is 5% ($1.94M)

under budget.

The key variances are as follows:

The Council and Councillors’ activity is 2% ($54K)

under budget primarily due to Grant Payments yet to be requested and lower

Councillor salary costs due principally to the short-term vacancy in the

Mararoa-Waimea Ward.

Other Activities expenditure is 45% ($528K) under budget as

the calculation of interest on reserves is calculated as a year-end

entry.

The Chief Executive activity is on budget. The funding

rounds for Stewart Island Visitor Levy to occur in May, as this expenditure was

not included in the budget any allocation will result in the group being over

budget for the year (although there will be income available for allocation).

The Environment and Community Group is 5% ($269K) under

budget. This is predominantly due to expenditure on the District Plan

being lower than anticipated at this stage of the year, with some costs being

incurred during April in relation to mediation. It is likely to be $400K

under budget at the end of the year.

Within Financial Services, expenditure is $324K (20%) under

budget, primarily due to the timing of audit services $106K and staff vacancies

of $115K.

Within the Information Management Group, expenditure is $37K

(2%) over budget. This is the result of $62K unbudgeted costs in relation to

the Information Management Strategy Review which is offset by reduced phone

calls and rentals ($27K).

Within the Policy and Community Group, expenditure is $76K

(6%) under budget due to no expenditure to date for Community Outcomes ($30K) and

lower than expected staff costs due to maternity leave.

Roading expenditure is currently 9% ($771K) over

budget. This is due to Network and Maintenance costs which are over

budget. These are to be monitored closely throughout the year but please note that it is forecast that the Repairs,

Maintenance and Capital Expenditure will be over budget at year end. This

is primarily driven by underspends in previous years and Council’s key

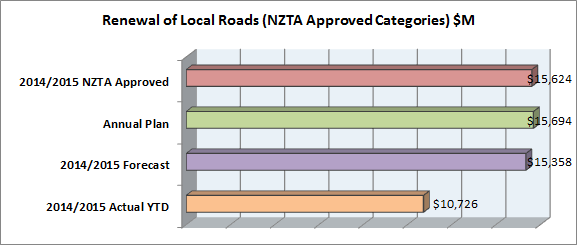

objective of maximising New Zealand Transport Agency approved funding.

Approval has been received by NZTA to shift funding from renewals to

maintenance.

The Services and Assets Group is 11% ($1.49M) under

budget. Key variances are as follows:

• District Water is $466K (20%) under budget as there has been minimal capital expenditure year-to-date

($270K actual v $785K budget).

• District Sewerage is $931K (26%) under budget. Year-to-date $2.7M actual versus $3.6M budget has been

completed.

• Water Services is $124K (12%) under budget predominately

due to less services of project consultant costs being required than budgeted.

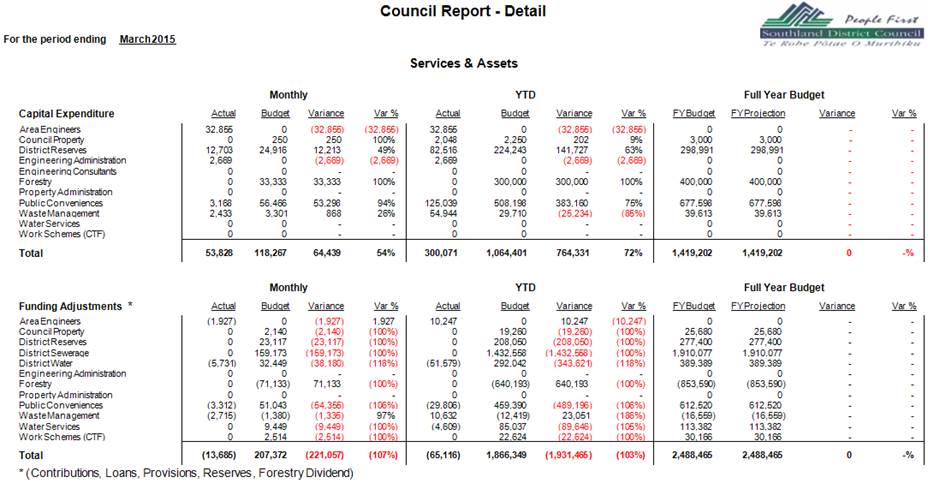

Capital Expenditure

Overall for the year-to-date, capital expenditure is 6%

($902K) under budget.

The key variances are as follows:

• Capital

Expenditure in the Chief Executive activity is over budget by $969K (63%)

due to the beginning of work for Stage 2 of the Around the Mountains Cycle

Trail.

• Environment

and Community is over budget by 60% ($85K). This is primarily due to an

additional vehicle purchase for animal control and the timing of the

replacement of a vehicle for environmental health.

• Information

Management capital expenditure is under budget by 69% ($155K) due to minimal

costs to date being incurred in the records improvement plan.

• Roading

capital expenditure is under budget by 9% ($1.03M) due to timing on planned

road renewal and pavement renewal. They are forecast to be $540K under

budget at year end.

• Services

and Assets are under budget by 72% ($764K) with minimal capital expenditure to

date on projects planned in public conveniences, district reserves and

forestry.

Funding Adjustments

Funding adjustments are significantly under budget as

typically ‘balancing’ of business units is not undertaken until the

end of the financial year.

Journals are being processed for reserve transfers,

predominantly in relation to vehicle movements, and loan draw-downs (ie for

project funding), throughout the year at the request of budget managers.

Key Financial Indicators

|

Indicator

|

Target*

|

Actual

|

Variance

|

Compliance

|

|

External Funding:

Non rateable income/Total income

|

>39%

|

37%

|

-2%

|

x

|

|

Working Capital:

Current Assets/Current Liabilities

|

>1.09

|

2.10

|

1.01

|

a

|

|

Debt Ratio:**

Total Liabilities/Total Assets

|

<0.73%

|

0.89%

|

0.16%

|

x

|

|

Debt To Equity Ratio:

Total Debt/Total Equity

|

<0.01%

|

0.00%

|

0.01

|

a

|

* All

target indicators have been calculated using the 2014/15 Annual Plan

figures.

** Excludes

internal loans.

Financial Ratios Calculations:

External Funding:

|

|

Non-Rateable

Income

|

|

|

|

Total Income

|

|

This ratio indicates the percentage of revenue received

outside of rates. The higher the proportion of revenue that the Council

has from these sources the less reliance it has on rates income to fund its

costs.

Working Capital:

|

|

Current Assets

|

|

|

|

Current

Liabilities

|

|

This ratio indicates the amount by which short-term assets

exceed short term obligations. The higher the ratio the more comfortable

the Council can fund its short term liabilities.

Debt Ratio:

|

|

Total Liabilities

|

|

|

|

Total Assets

|

|

This ratio indicates the capacity of which the Council can

borrow funds. This ratio is generally used by lending institutions to

assess entities financial leverage. Generally the lower the ratio the

more capacity to borrow.

Debt to Equity Ratio:

It indicates what proportion of equity and debt the Council

is using to finance its assets.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

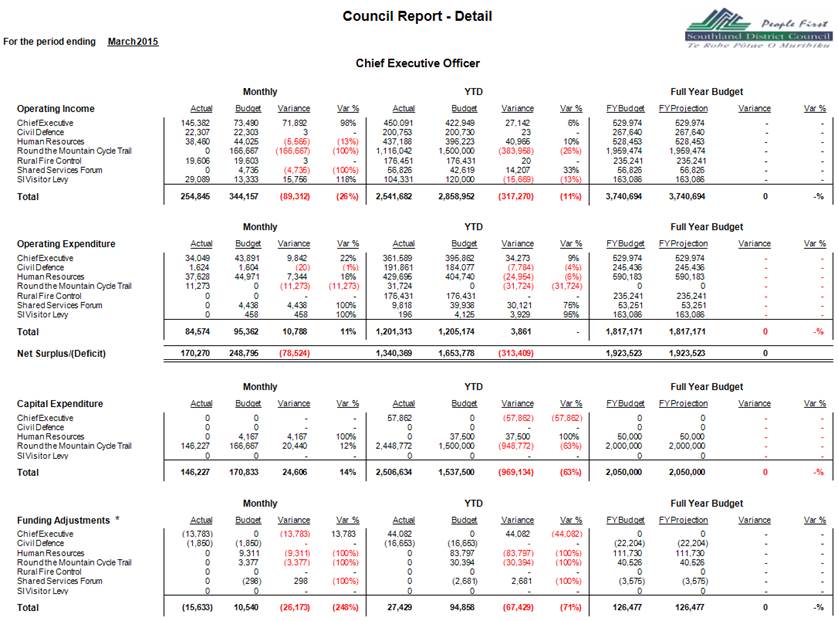

CHIEF EXECUTIVE COMMENTARY

For the year-to-date, income is under budget by $317K

(11%). Expenditure is under budget by $4K, therefore resulting in a net

year-to-date position of $313K under budget.

Chief Executive

Income in this business unit is $27K (6%) over budget which

is due to proceeds on an unbudgeted vehicle sale $14K and rates penalties

income $14K. Expenditure is $34K (9%) under budget, primarily due to

staff costs $66K under budget. This is offset by project consultant fees

$31K.

Civil Defence

Income is on budget. Expenditure is $8K (4%) over

budget due to the Emergency Management Southland grant being slightly higher

than was budgeted. It is anticipated to be $10K over budget at year end.

Human Resources

Income is $41K (10%) over budget. Expenditure

year-to-date is $25K (6%) over budget, due to training costs $51K offset by

survey expenses $20K, consultant costs $13K and staff costs $10K. As this

activity is internally funded, the increased expenditure impacts directly on

income.

Around the Mountains Cycle Trail

Income is $384K (26%) under budget due to substantial

invoicing to the Ministry being completed last financial year.

Expenditure is $32K over budget and capital expenditure over budget by $949K

with work being undertaken on Stage 2.

Rural Fire Control

Income and Expenditure is on budget for the year.

Shared Services Forum

Income is $14K (33%) over budget due to the timing on

contributions. Expenditure for year-to-date is under budget by $30K

(75%), with low activity for the year.

Stewart Island Visitor Levy

Income is $16K (13%) under budget. With the cruise

ship period completed, income is expected to be under budget at year end.

Expenditure is $4K under budget as the Allocations Committee meeting is set to

occur in early May.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

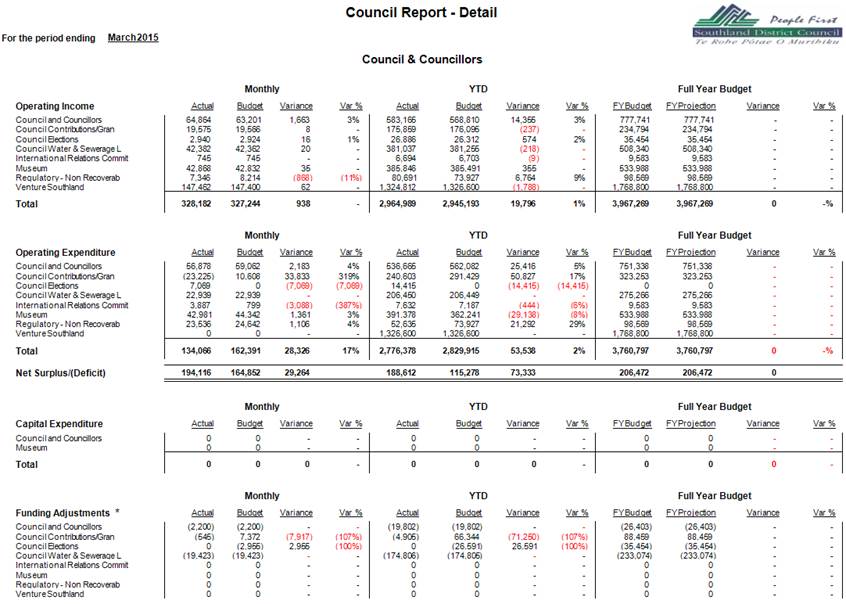

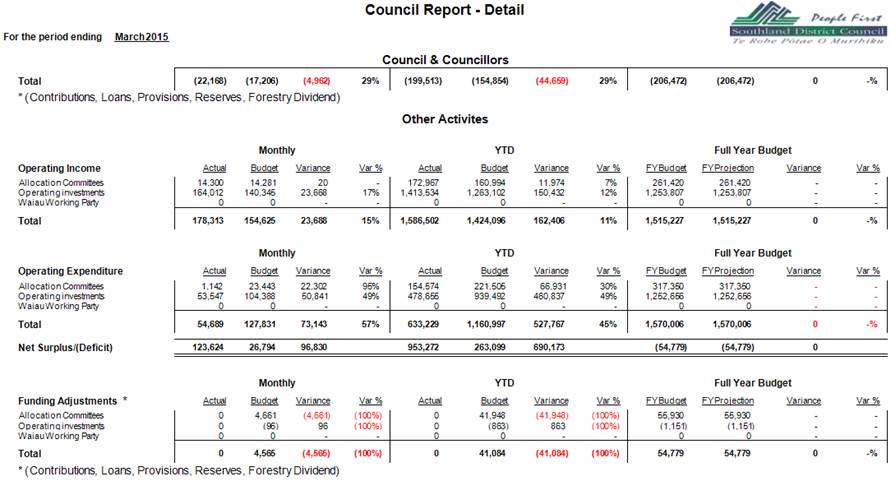

Council and Councillors’ Commentary

For the year-to-date, income is $20K (1%) over budget.

Expenditure is under budget by $54K (2%), therefore resulting in a net

year-to-date position of $73K over budget.

Council and Councillors

Income is $14K (3%) over budget as a result of unbudgeted

income from internal catering. Expenditure is under budget by $25K (5%)

primarily due to Councillors’ salaries of $14K, Travel $5K and Youth

Council costs $10K, however, we are anticipating higher year-end expenditure in

relation to Leadlab for the Youth Council.

Council Contributions/Grants

Income is on budget for the year-to-date. Expenditure

is under budget by $51K (17%) due to grant payments yet to be requested and the

upcoming grant allocation round.

Council Elections

Income is on budget. Expenditure is $14K over budget

due to the Mararoa-Waimea Ward Councillor by-election.

Council Water and Sewerage Loans

Income and expenditure is on budget for the year-to-date.

International Relations Committee

Income is on budget for the year-to-date. Expenditure

is $444 (6%) over budget with attendance at the Sister Cities Conference in

March. It is expected to align with budget by the end of the year.

Museum

Income is on budget. Expenditure is over budget $29K

(8%) due to timing on the Museum Trust Board Levy, it is expected to be on

budget at the end of the year.

Regulatory - Non-Recoverable

Income is $7K (9%) over budget for the year-to-date.

Expenditure is under budget by $21K (29%) as a result of minimal expenditure to

date.

Venture Southland

Income and Expenditure is on budget for the year-to-date.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

OTHER

ACTIVITIES’ COMMENTARY

Allocations Committee

Income is $12K (7%) over budget due to timing of grants

received. Expenditure is under budget by $67K (30%) due to the timing of

grant payments.

Operating Investments

Currently, the majority of

Council’s reserves are internally loaned by Council or its local

communities for major projects. Council has set the interest rate to be

charged on these loans as part of its Long Term Plan process and interest is

being charged on a monthly basis on all internal loans drawn down at 30 June

2014.

|

Activities Performance

Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

ENVIRONMENT AND

COMMUNITY COMMENTARY

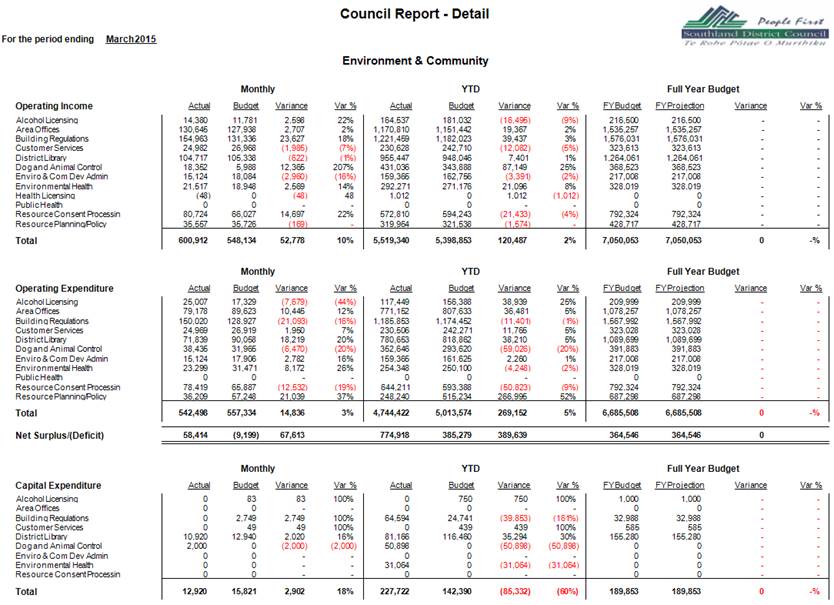

Overall monthly income for March 2015 was $53K (10%)

ahead of budget ($601K actual versus $548K budget).

Key features of this month’s income were that Building

Consent, Resource Consent and Animal Control income were well ahead of budget

by $24K (18%), $15K (22%) and $12K (207%) respectively, reflecting increased levels

of activity and values, and in the case of Animal Control recovery around

infringements.

This is a positive turn-around from February when income was

6% below budget.

Overall March 2015 monthly expenditure for the

Environment and Community Group was $15K (3%) below budget ($542K actual versus

$567K budget).

Most departments were below budgeted expenditure, reflecting

a close focus on spending.

The Resource Planning/Policy area was underspent by $21K

(37%) with less expenditure than anticipated on the District Plan

project.

Conversely, the Building Control area was $21K (16%)

overspent, due primarily to professional services and legal costs exceeding

budgets.

Overall YTD Summary

Overall YTD Income at the end of March 2015 for the

2014/15 financial year is $120K (2%) ahead of budget, at $5.5M actual versus

$5.4M budget.

Overall YTD Expenditure at the end of March 2015 of the

2014/15 financial year is $269K (5%) below budget at $4.7M actual versus $5.0M

budget.

The Resource Planning/Policy area is significantly under

budget year-to-date, but it is likely that further costs will be incurred in

the Environment Court appeal/mediation process throughout the remainder of the

year.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

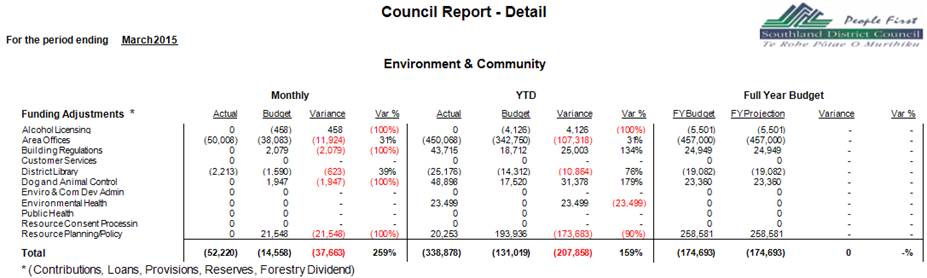

FINANCIAL

SERVICES COMMENTARY

Income is $295K (18%) under budget. As this activity

is internally funded, the reduced expenditure impacts directly on income.

Expenditure is $324K (20%) under budget. This is

primarily due to the following:

• The

timing of audit services ($106K).

• Vacancies

in the finance team ($185K) offset by an increase in consultants’ costs

to assist with workload ($15K).

• Visa/MasterCard

charges currently under budget ($11K).

• As

a result of the material damage insurance review costs related to insuring water

and wastewater, above ground assets have now been correctly coded to the water

and waste business units. This has resulted in actual costs being less

than budgeted by $45K.

At year end, it is expected that

the business unit will remain under budget by approximately $200K due to the

above.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

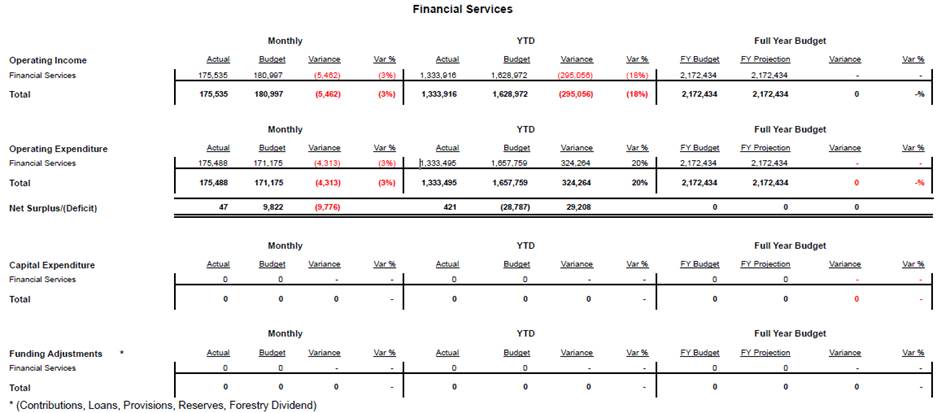

INFORMATION

MANAGEMENT COMMENTARY

For the year-to-date, income is $100K (5%) over

budget. Overall expenditure is $37K (2%) over budget, resulting in a

positive variance of $63K.

Information Management

Income is $68K (6%) over budget, predominantly due to

internal photocopying charges $34K and internal computer hire relating to

additional hardware $29K. Expenditure is $49K (5%) over budget.

This related primarily to consultants’ costs $62K as a result of

unbudgeted costs in relation to the IM Strategy Review.

Knowledge Management

Income is $6K (1%) over budget. Expenditure is $2K

over budget, this is due to postage costs $9K and software licence fees

$12K. This is offset by internal computer hire costs $10K and staff costs

$12K under budget. As this activity is internally funded, the increased

expenditure impacts directly on income.

Property and Spatial Services

Income is $26K (10%) over budget. Expenditure is $14K

under budget due to timing on aerial photography costs $51K; this is offset by

software licence fees $33K, consultant costs $12K and staff costs $8K.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

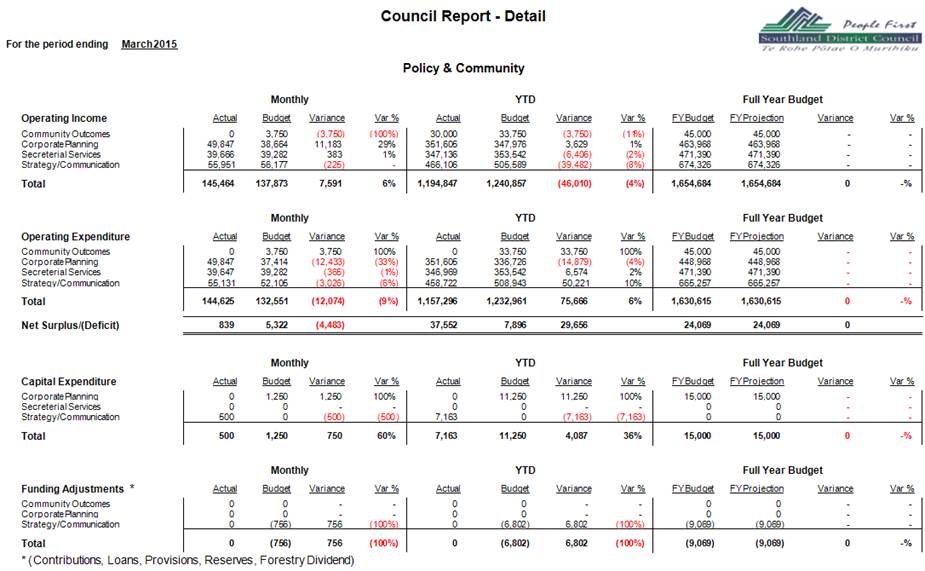

POLICY AND

COMMUNITY COMMENTARY

Income for the year-to-date is $46K (4%) under budget.

Expenditure for the year-to-date is $76K (6%) under budget. The net

result for the year-to-date is a surplus of $38K against a forecasted surplus

of $8K, a positive variance of $30K.

Community Outcomes

Income is on $4K under budget. Expenditure is under

budget $34K as no projects relating to the Our Way Southland Outcomes have been

identified in the current period.

Corporate Planning

Income is $4K (1%) over budget. Expenditure is $15K

(4%) over, due to additional costs relating to the Long Term Plan.

Secretarial Services

Income is $6K (2%) under budget. Expenditure is $7K

(2%) under budget predominately due to training costs $4K and internal

photocopying charges $2K. As this activity is internally funded, the

reduced expenditure impacts directly on income.

Strategy/Communication

Income is $39K (10%) under budget. Expenditure is

underspent by $50K (11%) predominately due to staff costs $38K and first

edition costs $16K below budget.

As this activity is internally funded the reduced expenditure impacts directly

on income.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

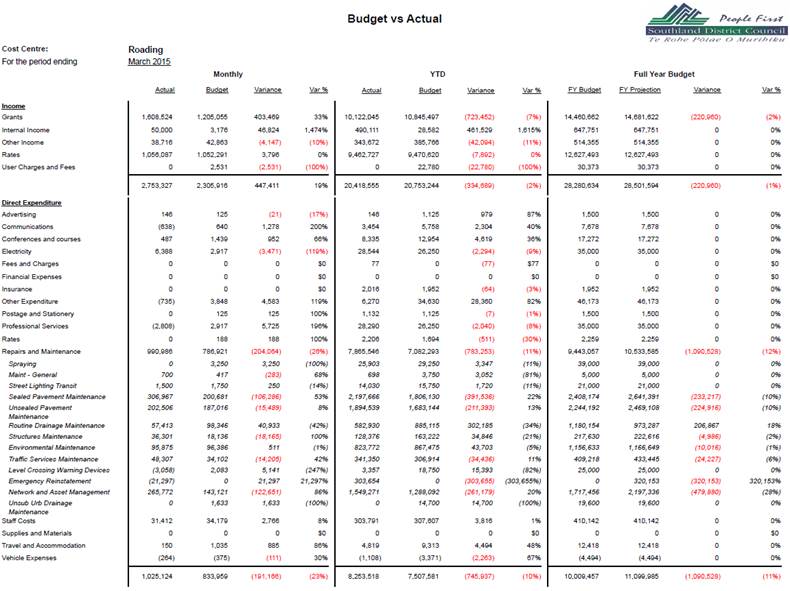

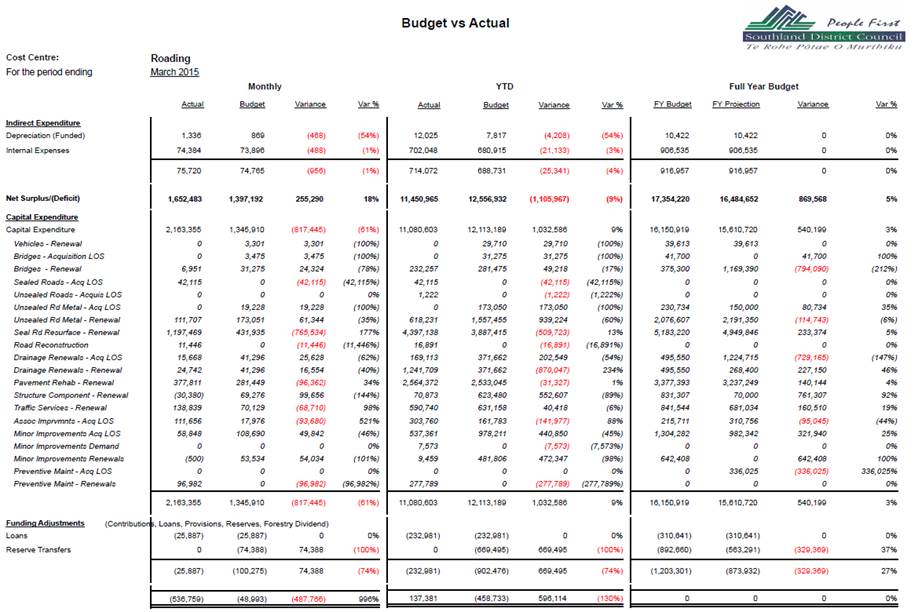

STRATEGIC

TRANSPORT

Overall Financial Performance

A continued strong focus on making sure we fully utilise

NZTA approved funding along with optimising “value for money”

remains a challenge.

• Council

Transport overheads are generally tracking in line with budgets.

• It

is forecasted that our Operations and Maintenance costs will be over budget at

year end. This will be partially offset by underspends in capital

expenditure and underspends in the previous two years. The forecasted

overspend can be also be contributed to unbudgeted emergency works projects

Stewart Island Slips and the Ohai Clifden Slip.

• Council

Transport Capital Expenditure is under budget primarily due to timing.

Final costs of resealing, rehabilitations, unsealed road metalling and bridge

renewal work are expected to occur over the coming months.

Please

note that we are forecasting that our Repairs, Maintenance and Capital

Expenditure will be over budget at year end. This is primarily driven by

underspends in previous years and our key objective of maximising New Zealand

Transport Agency approved funding.

|

Key

|

|

|

Largely on

Track

|

|

|

Monitoring

|

|

|

Action

Required

|

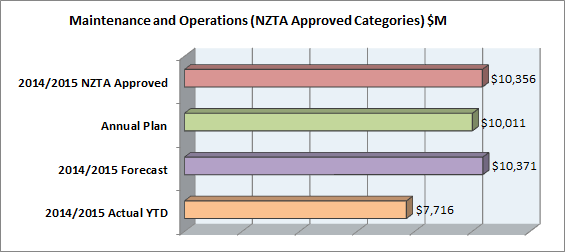

Maintenance and Operations:

|

Financial Tracking vs Plans

|

|

YTD

|

Forecast

|

Annual Plan

|

NZTA Approved

|

|

75%

|

74%

|

77%

|

75%

|

Maintenance and Operation costs are currently over

budget. This is due to:

A

holistic approach to Maintenance Management has seen Sealed Pavement and

Unsealed Pavement Maintenance being over budget but offset with underspends in

other activities. Plus we are bringing forward from 2015/16 our bi-annual

data collection into 2014/15.

*

Note that Council can only claim 30% of urban

drainage. Unsubsidised work has being excluded from this forecast.

Council

have had approval from NZTA to shift funding from renewals to maintenance.

Renewals and Minor

Improvements:

|

Financial Tracking vs Plans

|

|

YTD

|

Forecast

|

Annual Plan

|

NZTA Approved

|

|

75%

|

70%

|

68%

|

69%

|

Renewals and Minor Improvement Commentary:

The above is highlighted in orange

as Transport is monitoring these costs closely driven by the current volatility

in the bitumen index.

It is expected that budgets will

align over the next couple of months.

Three Year Programme:

As we have had formal approval from NZTA for more funding for

the Lower Hollyford Road, this will not impact Local

share as it is 100% funded by NZTA.

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

SERVICES AND

ASSETS (Excluding Roading)

COMMENTARY

Income

Overall Services and Assets

(excluding Roading) actual income is $91K (1%) over year-to-date budget

($13.0M). This is primarily driven by Forestry income $108K over budget.

Key highlights are:

• District Reserves is $14K under budget as some reserve

transfers for Curio Bay have yet to be actioned.

• Engineering Consultants is $57K (9%) under budget. As

income is fully recovered and driven by

expenditure levels the reduced expenditure impacts directly on

income.

• Overall

Forestry income received is $108K (6%) over budget. This is expected to

be the position at the end of the year as all

harvesting has been completed for this financial year. This is predominantly due to harvesting in Waikaia

$935K over budget. This is offset by Dipton Forest $460K and Ohai Forest

$366K under budget.

Operating Expenditure

Actual operational expenditure for

Services and Assets year-to-date is $1.41M (11%) under budget.

Key highlights are:

• District Water is $466K (20%) under budget as there has been minimal capital expenditure year-to-date

(270K actual versus $785K budget).

• District Sewerage is $931K (26%) under budget. Year-to-date $2.7M actual versus $3.6M budget has been

completed.

• Water Services is $124K (12%) under budget predominately

due to less services of project consultant costs being required than budgeted.

• Currently

the Engineering Consultants’ business unit is

$57K (9%) under budget.

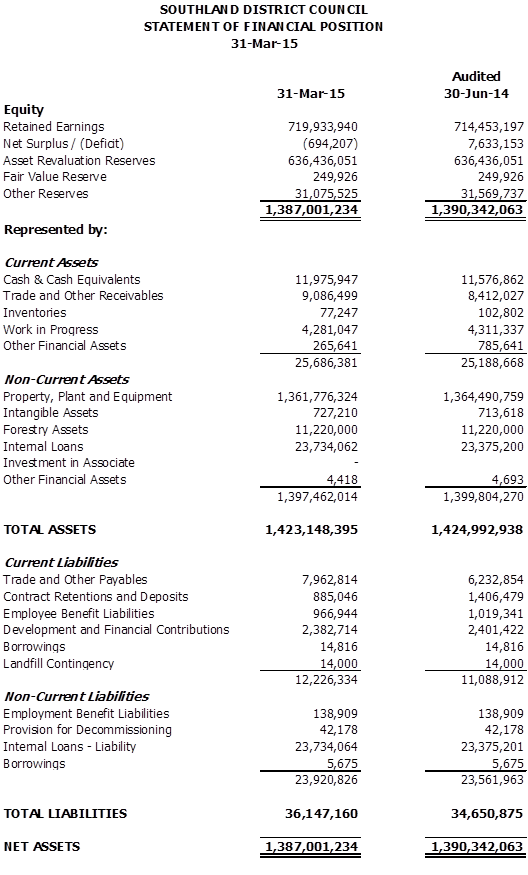

Statement of Financial Position

COMMENTARY

The balance sheet as at 30 June

2014 represents the audited balance sheet for activities of Council (ie

excludes SIESA and Venture Southland). The financial position at

31 March 2015 is before year-end adjustments and only for the activities of

Council.

External borrowings have still not

been required, with internal funds being used to meet obligations for the

year-to-date.

|

|

|

|

|

Susan McNamara

MANAGEMENT ACCOUNTANT

|

|

|

|

|

|

|

Activities

Performance Audit Committee

03 June 2015

|

|

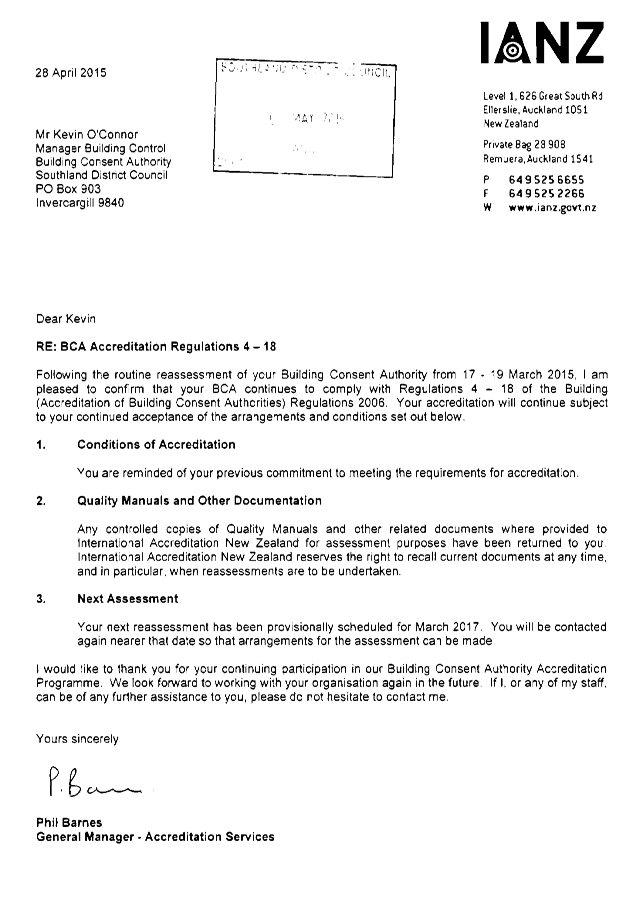

Report to Activities Performance Audit Committee on

outcome of 2015 International Accreditation New Zealand (IANZ) Reaccreditation

Audit of Southland District Council Building Control Section

Record No: R/15/5/8389

Author: Bruce

Halligan, GM - Environment and Community

Approved by: Steve Ruru,

Chief Executive

☐

Decision ☐ Recommendation ☒ Information

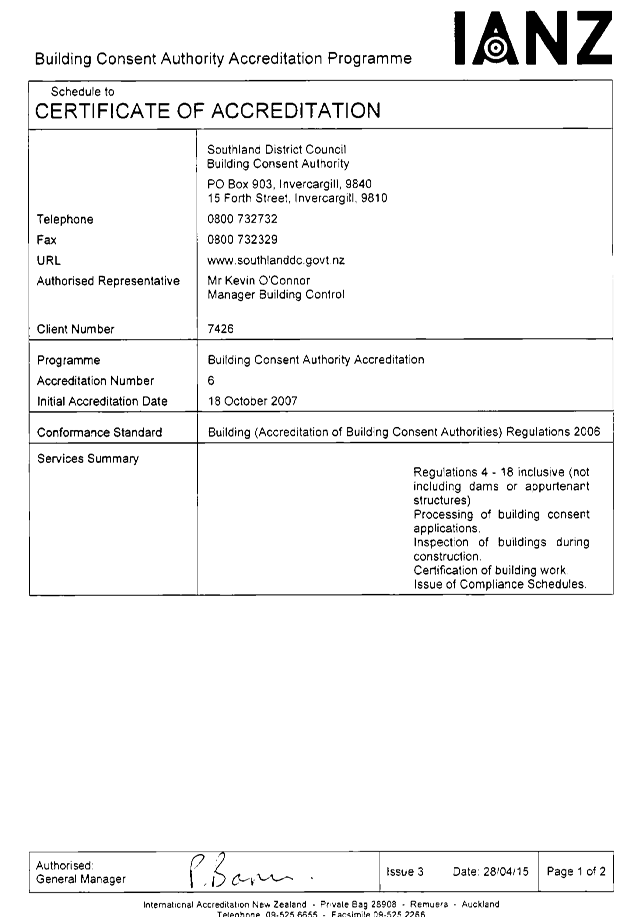

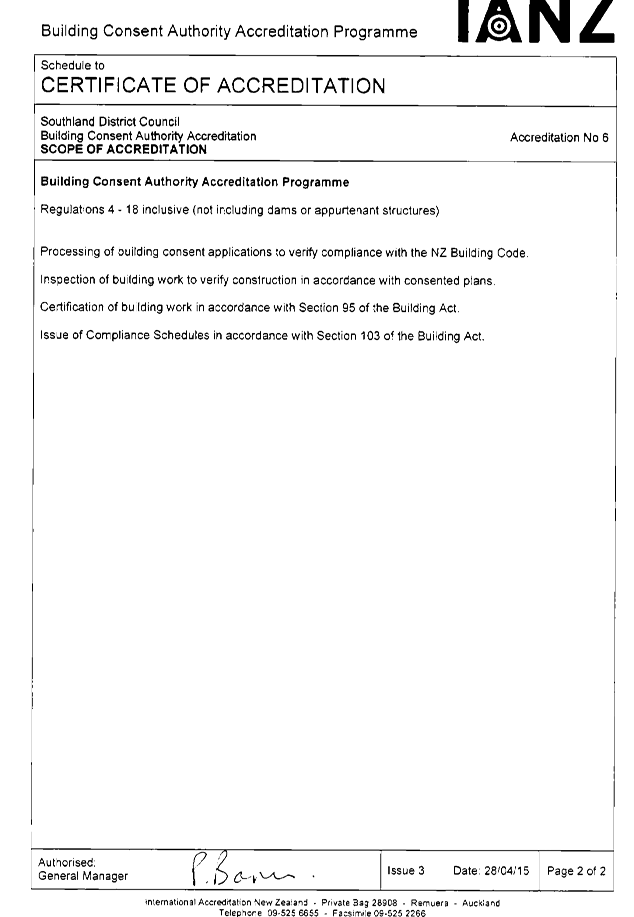

1 This

report provides information for the Committee on the outcome of the recent

International Accreditation New Zealand (IANZ) 2015 reaccreditation audit of

the Southland District Council (SDC) Building Control section.

2 I

am pleased to report that the SDC Building Control section was reaccredited for

a further two year period, with no Corrective Actions Required (known as CARs).

3 This

is a very pleasing result, not only for the Building Control Section but also the

wider organisation.

4 IANZ

undertakes an intensive audit process of all Building Control Authorities

(BCAs) on a two yearly basis. This audit process involves not only a

thorough review of relevant documentation and processes, but also a field

element where IANZ assessors accompany some staff in the field to observe their

inspection processes first-hand.

5 For

any Council to be able to issue building consents and Code Compliance

Certificates under the Building Act 2004, that Council must be IANZ-accredited.

6 Councillors

will no doubt be aware that some other local authorities elsewhere have lost

their IANZ accreditation, which has meant that they have then had to make

alternative arrangements for other councils to process consents on their

behalf, with associated additional costs.

7 SDC

has been accredited by IANZ since 2007, being one of the first councils to

achieve this. During March 2015, the IANZ team was on site undertaking

the reassessment/ reaccreditation audit.

8 In

such an audit, IANZ has the option of either reaccrediting, or requiring

corrective actions to be taken (CARs, as referred to above) prior to

reaccreditation, or not reaccrediting at all.

9 It

is a great credit to Kevin O’Connor and the whole of the Building Control

team that SDC was reaccredited for a further two years with no corrective

actions required, with March 2017 being the next reassessment audit.

10 While

I take no credit for the reaccreditation, as Group Manager with responsibility

for the Building Control section, I am really proud of the Building Control

team for this significant achievement. This can also give confidence to

our customers that SDC has thorough processes and technical competency in the

Building Control area, which is very important as it is one of the key

potential liability areas for any Council.

11 IANZ

has made a series of strong recommendations which are NOT CARs, but rather are

recommended areas for future improvement. These strong recommendations

are very useful for the continuous improvement process. Mr O’Connor

and the team will be working at taking the actions as specified in the schedule

attached in Appendix B to address these strong recommendations.

12 Mr

O’Connor will also be present at the APAC meeting to respond to any

queries Committee members may have in that regard.

|

Recommendation

That the Activities

Performance Audit Committee:

a) Receives

the report titled “Report to Activities Performance Audit Committee on

outcome of 2015 International Accreditation New Zealand (IANZ)

Reaccreditation Audit of Southland District Council Building Control

Section” dated 19 May 2015.

|

Attachments

a IANZ

BCA Accreditation Regulations 4-18 has been achieved View

b Follow

up from IANZ re-assessment of 17 - 19 March 2015 View

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Activities

Performance Audit Committee

|

03 June 2015

|

|

Follow up

from IANZ re-assessment of 17 - 19 March 2015

|

|

Notes:

· Corrective

Actions are to be cleared by the specified date from International

Accreditation New Zealand (IANZ).

· Strong

recommendations are to be actioned before the next biennial IANZ

re-assessment.

· Recommendations

are to be considered for actioning before the next biennial IANZ

re-assessment.

· Responses

are to be communicated to staff in monthly meeting agenda after completion.

· Responses

are recorded in section QA1 of the QAS Manual after completion.

|

|

Corrective

Actions

|

|

Action required/recommended

|

Proposed response

|

Accepted

yes/no

|

Date to be

actioned

|

Date

completed

|

|

No corrective actions

identified by IANZ

|

N/A

|

N/A

|

N/A

|

N/A

|

|

Strong

Recommendations

|

|

Action required/recommended

|

Proposed response

|

Accepted

yes/no

|

Date to be

actioned

|

Date

completed

|

|

It is

strongly recommended that the BCA always ensures that hard copy and

electronic copies of public information are the same version.

|

The Building Consent

Application Guide is to be reviewed and re-printed in hardcopy version.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA consent processing checklists be revised to

ensure they prompted review of producer statements and compliance schedule

information.

|

Electronic processing

check-sheets are to be reviewed to ensure that they prompt a review of

producer statement and compliance schedule information.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA ensures they do not include inappropriate

“advice notes” on consents.

|

Training on appropriate use

of construction prompts is to be undertaken at a monthly meeting.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCAs CCC procedures (checklist) prompt the BCO

to review Producer Statements and Third Party Certificates to establish full

compliance with the Building Consent.

|

Electronic processing

check-sheets are to be reviewed to ensure they prompt a review of producer

statement and compliance schedule information.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA ensures they do not issue generic

compliance schedules, or include any irrelevant standards on compliance

schedules.

|

Compliance schedule processes

are to be reviewed to require as much system information as possible is

provided upfront at consent processing stage so relevant standards are

referenced. The compliance schedule template is also to be reviewed.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA ensures that the monitoring of the

application of training is targeted to review the application of training

received.

|

A training plan - outcome

form is to be established to record application of training.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA describes in their procedures the processes

that they used to ensure contractors (such as engineers, the individual with

specialist processing skills, and the individual that performed competency

assessments, internal audits and training needs assessment) were technically

competent, both when first engaged, and at regular (annual) review of

competency.

|

QAS Manual section CA7

relating to contractors is to be reviewed to ensure provision is made for

regular review technical competency.

|

yes

|

01/07/15

|

|

|

Strong

Recommendations

|

|

Action required/recommended

|

Proposed response

|

Accepted

yes/no

|

Date to be

actioned

|

Date

completed

|

|

It is

strongly recommended that the BCA revise and implement procedures to require

contractors to provide technically appropriate outcomes.

|

QAS Manual section CA7 referenced

SLA template is to be amended to include reference to technically appropriate

outcomes.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA revise and implement procedures to require

contractors to demonstrate compliance with an agreed level of quality

assurance.

|

QAS Manual section CA7 SLA

template is to be amended to require contractors to demonstrate they are

meeting agreed level of quality assurance.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA revise its contractor procedures to require

the BCA to review the appropriateness of technical outcomes provided by

contractors.

|

QAS Manual section CA7 SLA

template is to be amended to require the BCA to review appropriateness of

technical outcomes.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA revise procedures to require the BCA to

review whether the contractor continued to comply with an agreed level of

quality assurance.

|

QAS Manual section CA7 SLA

template is to be amended to require the BCA to review contractors agreed

level quality assurance is being met.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA revise and implement procedures to require

the BCA to mark as superseded out-of-date versions of standards and product

specifications.

|

Archived hardcopy technical

information folders are to be stamped as “Superseded”.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA revise procedures (property file checklist)

to record where documents are located (i.e. hard copy or electronic file).

|

Form KM 3 Building Consent

Coversheet is to be amended to record whether documents are also recorded

electronically.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA describe somewhere (possibly in job

description) the responsibilities of the Quality Manager and refer in the

Quality Manual to where the responsibilities are described.

|

The job description for the

quality manager is to be amended to include quality assurance

responsibilities.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA specify (in the Quality Manual) the role of

the quality assurance person and describe somewhere (possibly in job

description) the responsibilities of the quality assurance person.

|

QAS Manual section CA8

technical/quality assurance manager reference will be amended to specify a

quality coordinator role additional to the quality manager role.

|

yes

|

01/07/15

|

|

|

It is

strongly recommended that the BCA specify in procedures where the BCA would

record the names of those who were exempt from holding a qualification.

|

QAS Manual section CA5 shall

be amended to require recording of BC office deemed exempted from obtaining a

qualification.

|

yes

|

01/07/15

|

|

|

Recommendations

|

|

Action

required/recommended

|

Proposed

response

|

Accepted

yes/no

|

Date to be

actioned

|

Date

completed

|

|

It is

recommended that the BCA revise and implement procedures to ensure they

require the BCA to periodically review all consents to see if there were any

that had slipped through the alert system that was designed to prompt the 11

and 12 month letters.

|

BC Admin to have a report

created to flag any granted consents that may slip passed the 12 month

follow-up stage.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA revise and implement procedures to ensure that they

require the BCA to periodically reviewed consents to see if there were any

slipping through the alert system that was designed to prompt the 23 and 24

month letters.

|

BC Admin to have a report

created to flag any granted consents that may slip passed the 24 month

follow-up stage.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA Compliance Schedule Template be reviewed to

facilitate the BCO’s when they are editing the Compliance Schedule.

|

The compliance schedule

process is to be reviewed to require as much system information provided

upfront at consent processing stage so relevant standards are referenced. The

compliance schedule template is also to be reviewed.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA revise their “Document Authorisation Table

(Dc2)” to record the limitations that individuals had in their

competencies as well as having those limitations specified in the individuals

competency assessments.

|

DC2 Document

Authorisation Table is to be amended to include competency limitations as

specified by Qualico in individual BC Officers competency assessments.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA revise their procedures to ensure they describe the

BCA’s current process whereby they monitored the timely completion of

all quality system functions on an on-going basis.

|

QAS Manual revision process

– record table shall be modified to strengthen the biennial review

process.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA ensure their contractor (performing competency

assessments) states that an individual is under “distant

supervision” only when they actually require supervision.

|

Instruction will be given to

Qualico that competency assessments are only specify distance supervision

where it is necessary for an individual competency rather than when it part

of the BCA process.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA revise their training procedure that discusses

supervision of site inspectors where the procedure inaccurately refers to

processing in two places.

|

QAS Manual section CA3 is to

be amended to reference supervision of site inspectors.

|

yes

|

01/07/15

|

|

|

It is

recommended that in anticipation of the possibility that the BCA may require

the services of other BCA’s, that SDC revise procedures to address

establishing and reviewing technical competency when engaging the services of

another BCA.

|

QAS Manual section CA7 is to

be amended to include the process for reviewing technical competency of BC

Officers engaged from elsewhere.

|

yes

|

01/07/15

|

|

|

It is

recommended that in anticipation of the possibility that the BCA may require

the services of other BCA’s, that the BCA revise procedures to specify

expectations in more detail for when making such agreements (work briefs)

with other BCA’s.

|

Investigate will be

undertaken with the Southern Cluster into the possibility of establishing a

work brief that is supplementary to the Resource Sharing Agreement.

|

yes

|

01/07/15

|

|

|

It

is recommended that the BCA revise procedures to require the BCA to secure

copies of relevant diplomas, degrees or certificates rather than just

records.

|

QAS Manual section CA3 for

SDC is to be revised to require for regular review of the G Drive individual

training records to ensure BCO’s are copying training certificates into

the training record register.

|

yes

|

01/07/15

|

|

|

It is

recommended that in anticipation of the possibility that the BCA may require

the services of other BCA’s, that the BCA revise procedures to require

other contracted BCA’s to supply records that demonstrate the

BCO’s have appropriate qualifications.

|

QAS Manual section CA7 is to

be amended to require engaged BC Officers to provide verification of

appropriate qualifications.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA may wish to consider sending moisture meters out for

servicing and calibration only when they read outside the range specified on

their dedicated moisture block.

|

Consider amending QAS Manual

section AD3 so SDC has the option is testing moisture meters in house and

only sending those failing the test to be sent away for calibration.

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA review its application of the terminology

“non-critical” in respect to measurements. The IANZ document

“Specific Criteria for accreditation of Building Consent

Authorities”, October 2012 specifies that “Measurements that are important

to demonstrate compliance with the Building Code through acceptable

solutions, alternative solutions, specifications etc.” are deemed

“Critical”.

|

QAS Manual section AD3 is to

be reviewed for critical applies to equipment such as moisture meters and

thermometers in terms of calibration against a certified reference device or

calibration by an external party .

|

yes

|

01/07/15

|

|

|

It is

recommended that the BCA may wish to consider including in procedures the

delegation of authorities from the Mayor and elected officials to the

Building Consent Authority Manager.

|

Existing delegations under

QAS Manual section CA8 are deemed sufficient.

|

no

|

n/a

|

n/a

|

|

It is

recommended that the BCA consider revising their procedures for continuous

improvements to ensure more than one person reviews proposed continuous

improvements from a quality assurance perspective.

|

Not deemed necessary.

|

no

|

n/a

|

n/a

|

|

It is

recommended that the BCA revise continuous improvement procedures to ensure

proposed continuous improvements are entered onto the register at the point

at the point at which it is decided to progress the improvement rather than

after it has been resolved. The register then becomes a useful tool to

monitor whether continuous improvements are being resolved in a timely

fashion.

|

QAS Manual section QA1

continuous improvement register is to be amended to include an initiated and

completion date for actioned corrective and preventative items.

|

yes

|

01/07/15

|

|

|

Activities

Performance Audit Committee

03 June 2015

|

|

Request for Council to Maintain Irthing Road, Five

Rivers

Record No: R/15/4/7505

Author: Joe

Bourque, Strategic Manager Transport

Approved by: Ian

Marshall, GM - Services and Assets

☒

Decision ☐ Recommendation ☐ Information

Purpose

1 The

purpose of this report is for the Activities Performance Audit Committee to

consider taking on the maintenance of a previously unmaintained section of

roadway.

Executive

Summary

2 Irthing

Road, located near Five Rivers, is partly maintained by Council. The maintained

section is between State Highway 97 (Mossburn Five Rivers Road) and the

intersection of Irthing and Mulholland Roads.

3 The

Strategic Transport Department has received a request from an adjacent land

owner to start maintaining the metalled roadway that extends beyond the

intersection of Irthing and Mulholland Roads. This existing road is largely

formed within the road reserve margins.

4 Based

on Council’s current Extent of Network Policy, maintenance of this

roadway is justified.

|

Recommendation

That the Activities

Performance Audit Committee:

a) Receives

the report titled “Request for Council to Maintain Irthing Road, Five

Rivers” dated 26 May 2015.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Approves

the Strategic Transport Department recommendation to maintain Irthing Road,

beyond the intersection of Mulholland Road in accordance with the Extent of

Network conditions of the Roading Policy.

|

Content

Background

5 The

road reserve extending north-west on Irthing Road beyond the Mulholland Road

intersection has never been maintained by the Southland District Council.

6 The

road reserve in question serves access to three different land owners and

ultimately terminates where access is gained to the applicants land. This also

serves as the sole access point to the Mt Bee Department of Conservation

recreational land. This DoC land includes the Mt Bee hut and several tracks for

outdoor enthusiasts covering mountain biking and tramping. There is an access

agreement in place between the applicant and DoC where access can be gained to

the conservation land by notifying the applicant beforehand.

7 SDC

Area Engineer Bruce Miller was initially approached by the land owners of 725

Irthing Road, Ben Walling and Sarah Flintoft. Ben and Sarah have owned this

land since 2007.

8 The

property at 725 Irthing Road was previously owned by Rayonier Forestry and was

planted out as a forestry block.

9 In

2006 a large wind event felled many trees within this forestry block and

Rayonier constructed a formed road along the paper road reserve and removed the

trees from this block before they went to waste. It is not known what condition

(if there even was a formed road) this road reserve was in before Rayonier

invested and upgraded the existing road.

10 Rayonier

constructed this roadway on the road reserve and they outlined this in a letter

addressed to Kevin McNaught of the SDC property department. The SDC contributed

no money towards this and made no agreement to maintain the road.

11 Bruce

Miller (Area Engineer) received an initial enquiry about Council taking over

maintenance of this road from Ben and Sarah, however he requested this be put

in writing to Council as to how the situation has changed and why Council

should now maintain the road.

12 As

part of the justification put forward, Ben Walling and Sarah Flintoft explained

that the road generates a lot of traffic due to the Department of Conservation

recreational land at the end of the road and that they themselves had invested

money in upgrading the road so they could access their own land (which is

landlocked by other land owners and the road reserve provides the only access

for them).

13 After

careful review and consideration of Councils Extent of Network conditions

within the Roading Policy and discussions with the Department of Conservation,

the Strategic Transport Department concluded it would be appropriate to put the

decision to the Activities Performance Audit Committee with the recommendation

of taking over maintenance of this section of road.

14 This

section of road would be classified and maintained as a low volume access road.

Issues

15 Responsibility

– maintenance of the currently unmaintained section of Irthing Road and

what level of service this should receive.

Factors to Consider

Legal and Statutory Requirements

16 There

are no statutory requirements in regards to this issue.

17 Council

are meeting the statutory requirement of providing legal access to 725 Irthing

Road with the road reserve in place. Council is obligated to provide legal

access, but not obligated to provide formed access.

18 The

road is currently formed largely over the legal road reserve and although it is

not currently maintained by Council, it is still Council land that they are

using and Council cannot avoid liability regardless of how safe or unsafe the

road currently is.

Community Views

19 No

formal community views have been sought up to this point of time, however

discussions have been held with Department of Conservation and how it affects

the community accessing facilities and features around Mt Bee. DoC had no

objections or concerns with Council potentially taking over maintenance of this

section of road.

Costs and Funding

20 To

upgrade the existing road to the required standard the Strategic Transport

Department estimate this cost to be in the vicinity of $11,000.

21 Ongoing

maintenance costs will range between $300-500 per year (based on 1-2 grades

maximum per year).

22 This

estimate was compiled with Councils Maintenance contractor SouthRoads and it is

deemed to be a reasonable estimate.

Policy Implications

23 Taking

over maintenance of this section of roadway would be in line with the Extent of

Network Policy currently in place.

24 The

Policy indicates Council should maintain a road where it is built within a

legal road reserve, it is the only reasonable access for more than one property

owner and where it provides the only reasonable access to a popular

recreational area.

Analysis

Options Considered

25 Option

1 – Council take over maintenance of Irthing Road beyond the intersection

of Mulholland Road

26 Option

2 – Council do not take over maintenance of Irthing Road beyond the

intersection of Mulholland Road

Analysis of Options

Option 1 – Council take over maintenance of

Irthing Road beyond the intersection of Mulholland Road

|

Advantages

|

Disadvantages

|

|

· Provide

a safe roadway surface for neighbouring land owners and community to access

the Mt Bee recreational reserve.

· Promoting

the area for the wider community with a safe access.

· This

option would be conforming to the current Extent of Network Policy.

|

· To

take over this section of roadway will come at a cost of approximately

$11,000

· Ongoing

maintenance costs in the vicinity of $300-500 per year.

|

Option 2 Council do not take over maintenance of

Irthing Road beyond the intersection of Mulholland Road

|

Advantages

|

Disadvantages

|

|

· No

up-front cost to upgrade the existing road ($11,000).

· No

ongoing maintenance costs ($300-500).

|

· Unable

to provide a safe roadway surface for users who currently use this road

· This

option would not be conforming to the current Extent of Network Policy

|

Assessment of Significance

27 This

decision is not seemed to be significant.

Recommended Option

28 The

Strategic Transport Department recommend that Irthing Road should be maintained

beyond the intersection of Mulholland Road to a level appropriate of a low

volume access road. Maintaining this section of roadway allows existing users a

more comfortable and reliable level of service to an area of recreational

interest.

Next Steps

- 3

June 2015 - Council to consider taking over the maintenance of Irthing Road

beyond the Mulholland Road intersection

- July

2015 - Notification of decision to affected land owners and Department of

Conservation

Attachments

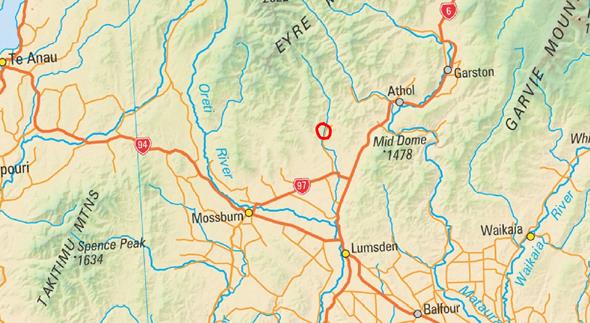

a Request

for Council to Maintain Irthing Road Five Rivers - Location Plan and Photos View

|

Activities

Performance Audit Committee

|

03 June 2015

|

Location Plan:

Extent of Requested SDC Maintenance:

Aerial View of Extent of Requested SDC

Maintenance:

Photos of Existing Track:

|

Activities

Performance Audit Committee

03 June 2015

|

|

Signs Maintenance Service

Record No: R/15/4/7342

Author: Joe

Bourque, Strategic Manager Transport

Approved by: Ian

Marshall, GM - Services and Assets

☒

Decision ☐ Recommendation ☐ Information

Introduction

and Background

1 The

signs maintenance contract will expire at midnight 30 June, 2015. At the

Activities Performance Audit Committee (APAC) meeting on 18 March 2015, it was

requested and resolved that APAC endorse delegated authority to the Group

Manager Services and Assets to investigate the most appropriate interim road

signs maintenance service, and to let a two year contract following a tender

process.

2 The

interim contract was to allow Council the time required to carry out and

complete the service level review currently being undertaken as required by

Section 17A of the Local Government Act 2002.

3 During

the investigation process and alterative option has been identified.

Proposal

4 During

the investigation process the option of incorporating the signs maintenance

services into the respective Road Alliance Contracts was considered and

explored.

5 This

option allows for a trial period on this service delivery method, with no long

term commitment from Council. The proposed period is from 1 July 2015 until 30

June 2016.

6 This

option is also likely to address the performance issues currently being

experience with the incumbent signs maintenance contractor based on the current

performance of the Alliances.

7 From

a cost perspective, this this option provides lower procurement costs as no

tendering process is required.

8 It

is also likely that through completing other maintenance activities that

non-value added activity can be reduced such as travel to and from site,

duplication of vehicles through maximising use of existing cyclic work vehicles

and providing opportunity to be more efficient in addressing non routine

activities.

|

Recommendation

That the Activities

Performance Audit Committee:

a) Receives

the report titled “Signs Maintenance Service” dated 22 May 2015.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Approve

delegated authority be granted to the Group Manager Services and Assets to

negotiate and incorporate the road signs maintenance activity within

the respective road maintenance contracts.

|

Attachments

There are no attachments for

this report.

|

Activities

Performance Audit Committee

03 June 2015

|

|

Southland

District Council 2015/2016 Resurfacing Contract - Contract 15/21

Record No: R/15/5/8622

Author: Joe

Bourque, Strategic Manager Transport

Approved by: Ian

Marshall, GM - Services and Assets

☒

Decision ☐ Recommendation ☐ Information

Purpose

1 The

attached report seeks endorsement from the Activities Performance Audit

Committee (APAC) for the proposed tendering methodology planned for the

2015/2016 Southland District Council’s (SDC) Resurfacing Programme.

This includes seeking delegated approval for the Chief Executive to let the

tender.

Executive

Summary

2 This

report covers the procurement methodology proposed for Contract 15/21 - SDC

2015/2016 Resurfacing. It is proposed that the full 2015/2016 resurfacing

programme that SDC is responsible for of approximately 950,000 m2 be

let under authority delegated to the Chief Executive as a single District-wide

one year contract.

|

Recommendation

That the Activities

Performance Audit Committee:

a) Receives

the report titled “Southland District Council 2015/2016 Resurfacing

Contract - Contract 15/21” dated 26 May 2015.

b) Determines

that this matter or decision be recognised as not significant

in terms of Section 76 of the Local Government Act 2002.

c) Determines

that it has complied with the decision-making provisions of the Local

Government Act 2002 to the extent necessary in relation to this decision; and

in accordance with Section 79 of the Act determines that it does not require

further information, further assessment of options or further analysis of

costs and benefits or advantages and disadvantages prior to making a decision

on this matter.

d) Endorses

the procurement methodology proposed for Contract 15/21 for the 2015/2016

Southland District Council Resurfacing Programme, and in particular:

i. The

work be let as a single contract.

ii. The

contract cover only the 2015/2016 programme.

iii. The

Chief Executive be delegated authority to let the contract subject to being

satisfied that it provides suitable value for money.

|

Content

Background

3 A programme of resurfacing requirements has been

developed for the 2015/2016 year which seeks to maintain the existing sealed

network from both an asset preservation and safety (skid resistance) point of

view.

4 This programme has sought to balance the risks of

seal failure, which can lead to pavement degradation and expensive repair, and

loss of skid resistance, which can increase crash risk, with the most efficient

use of the available resurfacing budget.

5 The work, involved in the contract, includes texturising

of preseal patching, temporary traffic management, sweeping, supply and

spraying of bitumen, supplying, placement and rolling of chips and the pavement

marking.

Issues

6 In

the past, contracts have been tendered for the SDC Resurfacing Programme based

on splitting the District into two or three areas and for either one or two

years.

7 Out of the last five resealing seasons, four of them have been

completed by a single contractor due to them winning all of SDC’s

contracts on offer.

8 Based on the analysis below, it is proposed to combine the full

Resurfacing Programme into a single one year contract for 2015/2016.

9 It is hoped that by having a single contract, this will increase

competition between the only two likely tenderers for this work.

10 It is also proposed to retain the bulk of the features of the

previous year’s performance based resurfacing contracts, which have

worked reasonably successfully.

11 This will include continuing to apply the standard NZTA cost

fluctuation formula. As always, predicting what this will do during the

season is very difficult as it depends on changes in bitumen prices and the

value of the $NZ versus the $US. Very few would have predicted the major

drop in bitumen costs which occurred in the 2014/2015 season.

12 Also similar to previous years, the cost of spraying the bitumen

will be included in with the supply, cart and laying of chips. This has

been done so that the bitumen cost is a supply only rate and can be more easily

identified when adjusting for cost fluctuations

13 It is proposed to let the tender using the Price Quality Method,

with a non-price weighting of 30%. This will allow the Tenderer

Evaluation Team to consider the quality aspects of the tenders submitted as

well as the price. This methodology has been used in the past and

received strong support from both local resurfacing contractors.

14 It is also proposed that authority be delegated to the Chief

Executive to let this contract.

This will enable the tender to be let as soon as possible after the tenders

close, enabling the successful tenderer to start the extensive detailed

preparation required.

Factors to Consider

Legal

and Statutory Requirements

15 The

project is part of the Southland District Council 2015/2016 Resurfacing

Programme.

It fits within the overall Land Transport Activity Management Plan and the Long

Term Plan.

16 No

unusual legal considerations are involved with this project. As with all

projects, but larger value projects in particular, there is the risk of a legal

challenge regarding the tender results from unsuccessful Tenderers. To

reduce this risk the Tender Evaluation Team will carefully follow the NZTA

procurement procedures.

17 The

Request for Tender will clearly state that the Principal reserves the right to

consider or reject any alternative tender, at the Principal’s sole

discretion.

Community

Views

18 The

final resurfacing treatments selected will take account of the existing seal,

road and environmental conditions, traffic loading, community expectations and

available sealing budget. This will result in use of smaller chips in

urban and built up areas where possible, to cut down traffic noise.

Costs

and Funding

19 The

budget for the 2015/2016 Resurfacing Programme is still be to confirmed, as the

full details of the New Zealand Transport Agency’s approval of Southland

District Council’s programme have not been provided. Initially a

budget of $4.5M has been set for the 2015/2016 Resurfacing Programme, including

the costs of professional services and SDC’s share of boundary roads

resealing being carried out by the Invercargill City Council.

The estimated value of the tender is approximately $4.45M including

contingencies, and depending on the final treatments selected.

20 Treatment

sites have been priorities to more easily allow adjusting the programme to

accommodate any budgetary changes, should it be required.

Policy

Implications

21 The

project is part of the Southland District Council 2015/2016 Resurfacing

Programme. It fits within the overall Asset Management Plan and the

Long Term Plan.

Analysis

Options Considered

22 In

developing the proposed procurement methodology a range of options have been

considered as detailed below:

Analysis of Options

Option 1 - Single Contract covering

the full District

|

Advantages

|

Disadvantages

|

|

· With

only one contract the tenderers only have one chance to win this work so they

have to put their best submission forward. This may maximise

competition in a market with just two players.

· There

is a slight reduction in contract administration with only one contract

rather than two.

|

· There

is risk to SDC in having its whole programme with one contractor if that

contractor does not perform. This risk has been successfully managed

over the last five years.

· The

unsuccessful tenderer has to find work elsewhere for a year.

|

Option 2 - Single Year Contact

|

Advantages

|

Disadvantages

|

|

· A

single year contract provides SDC with greater flexibility to consider the

outcome of the project delivery review currently being carried out and to

monitor the effects of the NZTA NOC Contract on the local market.

· This

also provides more opportunity to better develop a longer term programme

using the latest SCRIM (skid resistance data), high speed data and condition

rating data.

· A

single year contract makes business less difficult for the unsuccessful

tenderer with a single contract covering all of SDC.

|

· There

is more work involved for all parties in tendering this contract each year.

· There

are fewer options for successful tenderers to gain the benefits of more than

one year of committed work.

|

Assessment of Significance

23 While

the size of this proposed contract is large, the proposed procurement through

an open tender process, utilising the budget in the Long Term Plan, means that

the letting of this contract is not significant in terms of Section 76 of the

Local Government Act.

Recommended Option

24 It

is recommended that the Activities Performance Audit Committee endorse the

procurement methodology proposed for Contract 15/21 for the 2015/2016 SDC